If you are planning to apply for a personal loan, home loan, or credit card, one of the first things banks check is your CIBIL score.

A CIBIL score plays a major role in deciding whether your loan application gets approved or rejected. It also affects the interest rate you receive and the loan amount you can get.

Many people in India hear terms like “credit score” or “CIBIL score” but do not fully understand what they mean.

In this beginner-friendly guide, you will learn what a CIBIL score is, how it works, why it matters, how banks use it, and practical tips to improve your score.

If you are new to loans, you can also read:

What Is a CIBIL Score?

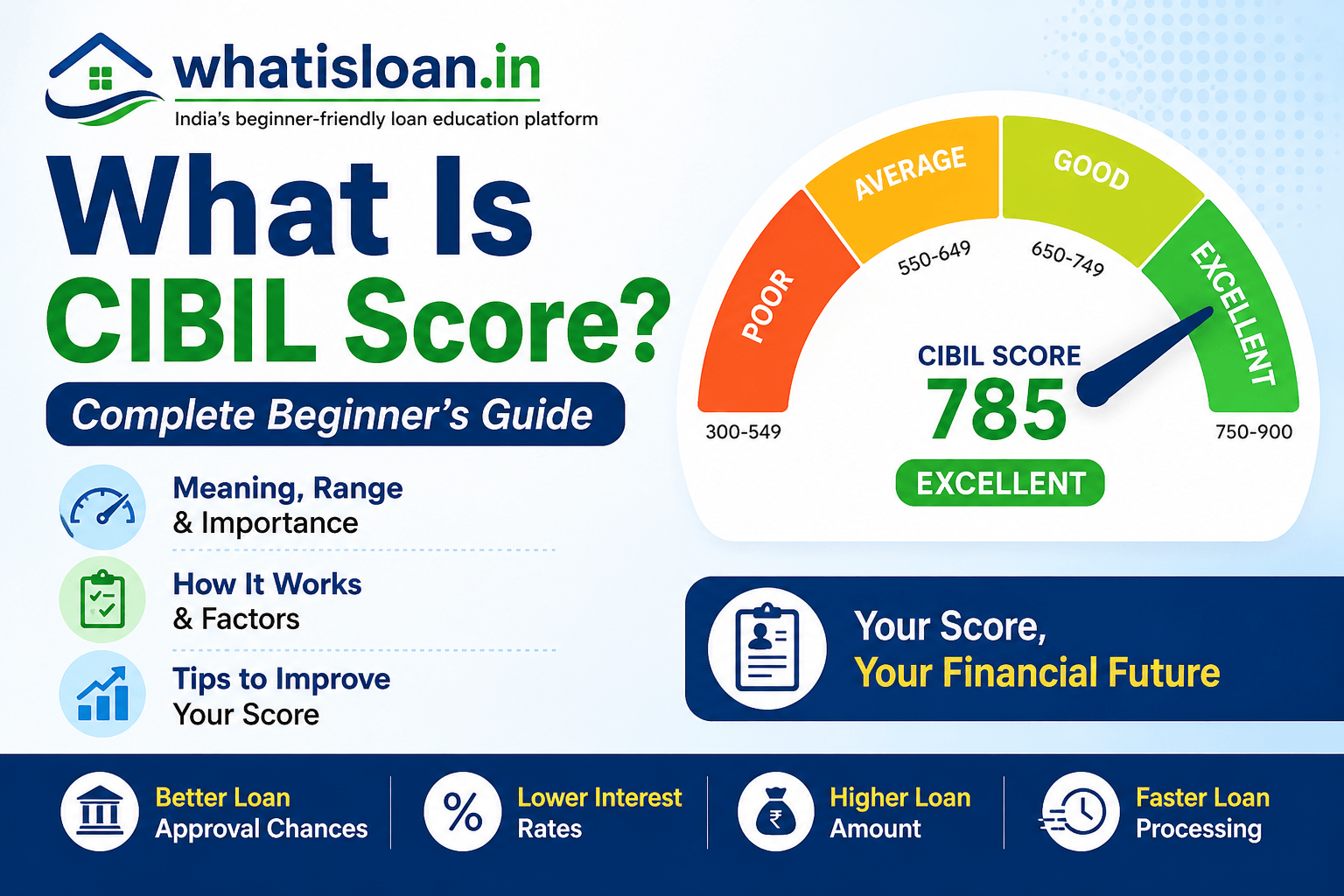

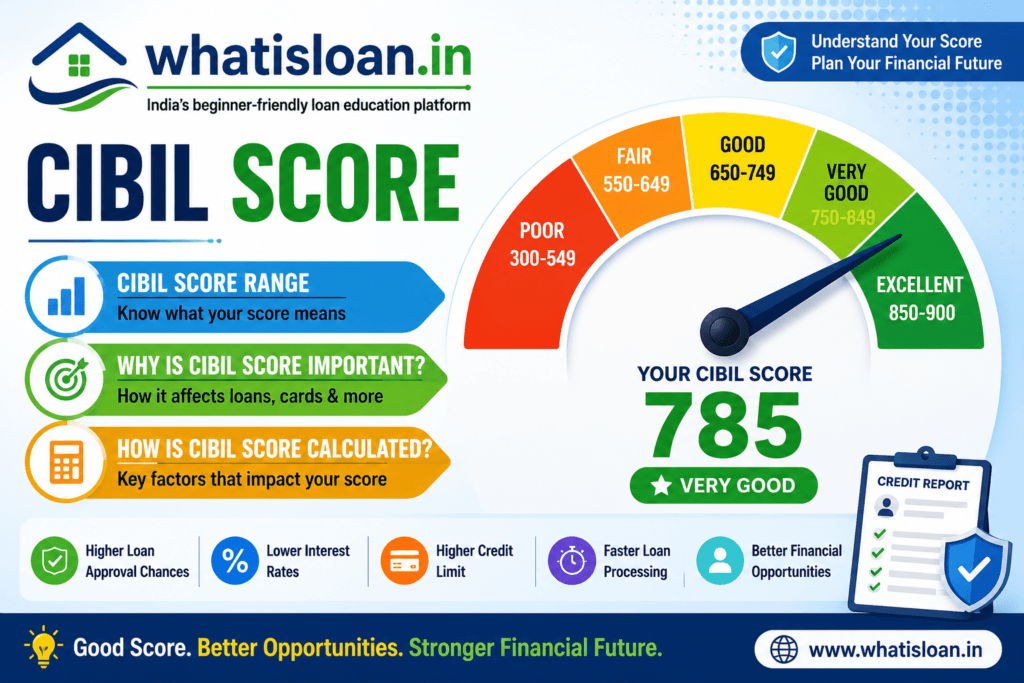

A CIBIL score is a three-digit number that represents your creditworthiness. It shows how responsibly you manage loans and credit cards.

The score usually ranges between 300 and 900.

A higher score indicates better financial discipline and increases your chances of getting loans approved easily.

Banks and NBFCs use this score to evaluate:

- Loan repayment behavior

- Credit history

- Existing debt

- Credit card usage

- Financial reliability

In simple words, your CIBIL score acts like a financial report card.

Check your CIBIL score here.

For example:

- A score above 750 is generally considered good.

- A lower score may reduce your loan approval chances.

What Is TransUnion CIBIL?

TransUnion CIBIL is one of India’s leading credit bureaus.

It collects financial data from:

- Banks

- NBFCs

- Credit card companies

- Financial institutions

Based on your repayment history and borrowing behavior, it generates your credit score and credit report.

Many people use the terms “CIBIL score” and “credit score” interchangeably.

However:

- CIBIL is the company

- Credit score is the number generated

CIBIL Score Range Explained

| CIBIL Score | Rating | Meaning |

|---|---|---|

| 750 – 900 | Excellent | High loan approval chances |

| 700 – 749 | Good | Usually approved |

| 650 – 699 | Average | Limited offers possible |

| 550 – 649 | Poor | Higher interest rates likely |

| Below 550 | Very Poor | Difficult loan approval |

Most banks prefer borrowers with scores above 750.

If your score is lower, lenders may:

- charge higher interest

- reduce loan amount

- ask for guarantor

- reject application

If you are comparing loan rates, read:

Fixed vs Floating Interest Rate

Why Is CIBIL Score Important?

Your CIBIL score affects multiple financial decisions.

1. Loan Approval

Banks use your score to decide whether to approve your loan application.

A higher score improves approval chances.

2. Interest Rates

Good scores can help you get lower interest rates.

Lower scores may result in expensive loans.

3. Credit Card Approval

Credit card companies also check your credit score before issuing cards.

4. Faster Loan Processing

Applicants with strong credit history often get faster approvals.

5. Better Loan Amount Eligibility

A healthy score can increase the loan amount you qualify for.

You can estimate your loan affordability using:

How Is CIBIL Score Calculated?

Several factors affect your CIBIL score.

Payment History

Paying EMIs and credit card bills on time has the biggest impact.

Late payments can damage your score significantly.

Credit Utilization Ratio

This means how much credit you use compared to your limit.

Experts usually recommend keeping usage below 30%.

Length of Credit History

Older credit history helps improve score stability.

Multiple Loan Applications

Applying for many loans in a short time can reduce your score.

Credit Mix

Having both secured and unsecured loans can positively affect your profile.

Examples:

- Home loan

- Car loan

- Personal loan

- Credit cards

What Is a Good CIBIL Score for Loans?

For Personal Loan

Most lenders prefer:

- 700 to 750+

For Home Loan

Banks usually prefer:

- 750 or higher

A higher score can help you secure lower home loan interest rates.

You can also use:

Plan Your Home Loan

How to Check Your CIBIL Score Online

You can check your score online easily.

Steps to Check CIBIL Score

- Visit official CIBIL website

- Enter your PAN and mobile number

- Complete OTP verification

- Access your credit report

You can usually get one free credit report every year.

Many banking apps and fintech platforms also offer free score checks.

How to Improve Your CIBIL Score

Improving your score takes time and financial discipline.

Pay EMIs on Time

Timely payments are one of the most important factors.

Keep Credit Card Usage Low

Avoid using your full credit limit regularly.

Avoid Multiple Loan Applications

Too many hard inquiries can reduce your score.

Maintain Old Credit Cards

Older accounts improve your credit history length.

Clear Outstanding Dues

Repay pending loans and overdue bills quickly.

Monitor Credit Report Regularly

Check for:

- wrong entries

- duplicate loans

- repayment errors

Common Reasons CIBIL Score Goes Down

Here are common mistakes that hurt credit score:

- Missed EMI payments

- Credit card defaults

- Loan settlements

- High credit card usage

- Frequent loan applications

- Closing old credit cards

- Loan defaults

Does Checking Your CIBIL Score Reduce It?

No.

When you check your own score, it is considered a “soft inquiry.”

Soft inquiries do not affect your score.

However, when banks check your report during loan processing, it becomes a “hard inquiry.”

Too many hard inquiries within a short time may slightly reduce your score.

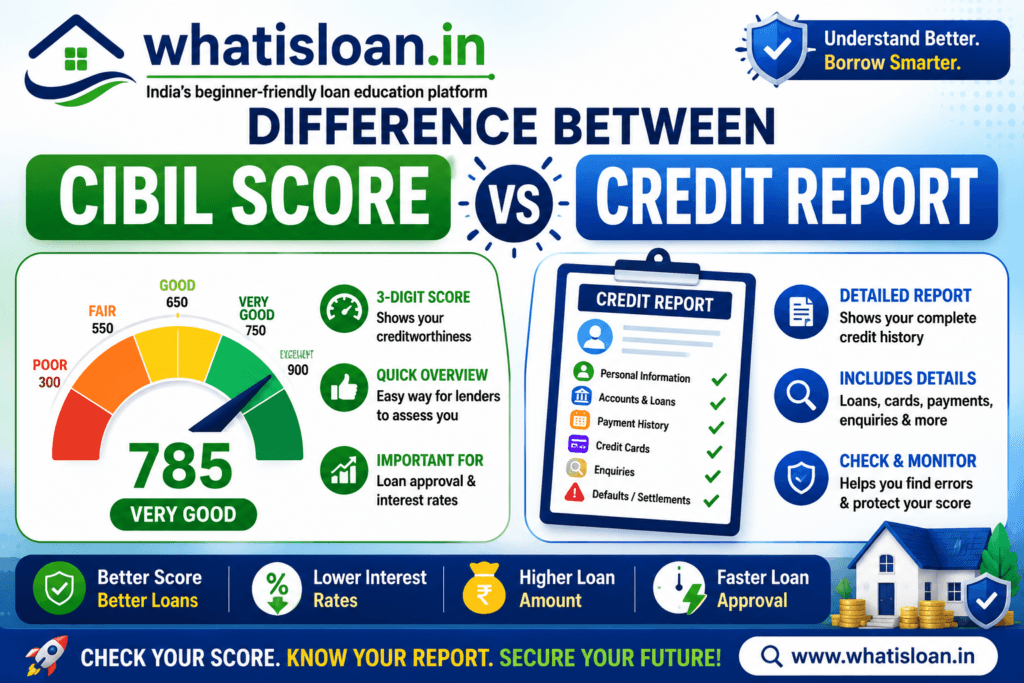

Difference Between CIBIL Score and Credit Report

| Feature | CIBIL Score | Credit Report |

| Meaning | Numeric score | Detailed report |

| Format | 3-digit number | Full credit history |

| Purpose | Quick evaluation | Detailed assessment |

| Includes | Creditworthiness | Loans, cards, repayment history |

Common Myths About CIBIL Score

Myth 1: Salary Affects CIBIL Score

Your salary itself does not directly affect your score.

Myth 2: Checking Score Lowers It

Self-checking does not reduce your score.

Myth 3: No Loan Means Excellent Score

Without credit history, lenders may not have enough data to assess you.

Myth 4: Closing Credit Cards Always Improves Score

Closing old cards may sometimes reduce credit history length.

Key Takeaways

- CIBIL score ranges from 300 to 900

- Higher score improves loan approval chances

- 750+ is generally considered good

- Timely EMI payments are very important

- Low score can increase interest rates

- Responsible borrowing helps maintain healthy score

FAQ Section

What is a good CIBIL score?

A score above 750 is generally considered good for loans and credit cards.

Can I get loan with low CIBIL score?

Yes, but approval may be difficult and interest rates may be higher.

How often does CIBIL score update?

Usually every 30 to 45 days depending on lender reporting.

Is 700 a good CIBIL score?

Yes, 700 is considered decent, though higher scores offer better benefits.

How can I improve my CIBIL score quickly?

Pay EMIs on time, reduce credit card usage, and avoid multiple loan applications.

Does EMI affect CIBIL score?

Yes. Timely EMI payments improve your score, while missed payments reduce it.

How much CIBIL score is required for home loan?

Most banks prefer 750 or higher for home loans.

Conclusion

A CIBIL score is one of the most important financial indicators for borrowers in India.

Whether you apply for a personal loan, home loan, or credit card, your credit score can affect approval chances, interest rates, and borrowing limits.

Maintaining a healthy score requires responsible financial habits like timely EMI payments, low credit utilization, and proper debt management.

A strong CIBIL score not only improves loan eligibility but also helps build long-term financial credibility.

Disclaimer

CIBIL score policies and lending criteria may vary between banks and financial institutions. Loan approval depends on multiple factors including income, employment, repayment capacity, and lender policies. Always verify the latest information directly with banks and official credit bureaus.