Buying a house is one of the biggest financial goals for many people in India. However, with rising property prices, purchasing a home with savings is not possible for most families. This is where a home loan becomes really helpful.

A home loan allows you to buy, build, or renovate a property by taking a home loan from a bank or financial institution and repaying it over time through monthly installments.

But what is a home loan exactly, and how does it work?

If you are planning to buy your first home, understanding home loans is very important. You should know about interest rates, EMI payments, eligibility criteria, tax benefits, and the risks involved before applying.

In this beginner-friendly guide, you will learn everything about home loans in simple language, including how they work, types of home loans, EMI calculation, tax benefits, and important tips before applying.

What Is a Home Loan?

A home loan is a secured loan offered by banks and financial institutions to help people buy, construct, renovate, or expand a house or property.

In simple words, the lender provides money for the property purchase, and the borrower repays the amount over a fixed period through monthly EMIs.

A home loan is called a secured loan because the property itself acts as collateral. If the borrower fails to repay the loan, the lender has the legal right to recover the amount by taking possession of the property.

Home loans usually come with:

- Large loan amounts

- Long repayment tenure

- Lower interest rates compared to personal loans

- Tax benefits under Indian income tax laws

The repayment tenure for home loans can go up to 30 years depending on the lender and borrower profile.

How Does a Home Loan Work?

Understanding how a home loan works can help you make better financial decisions.

Home Loan Application Process

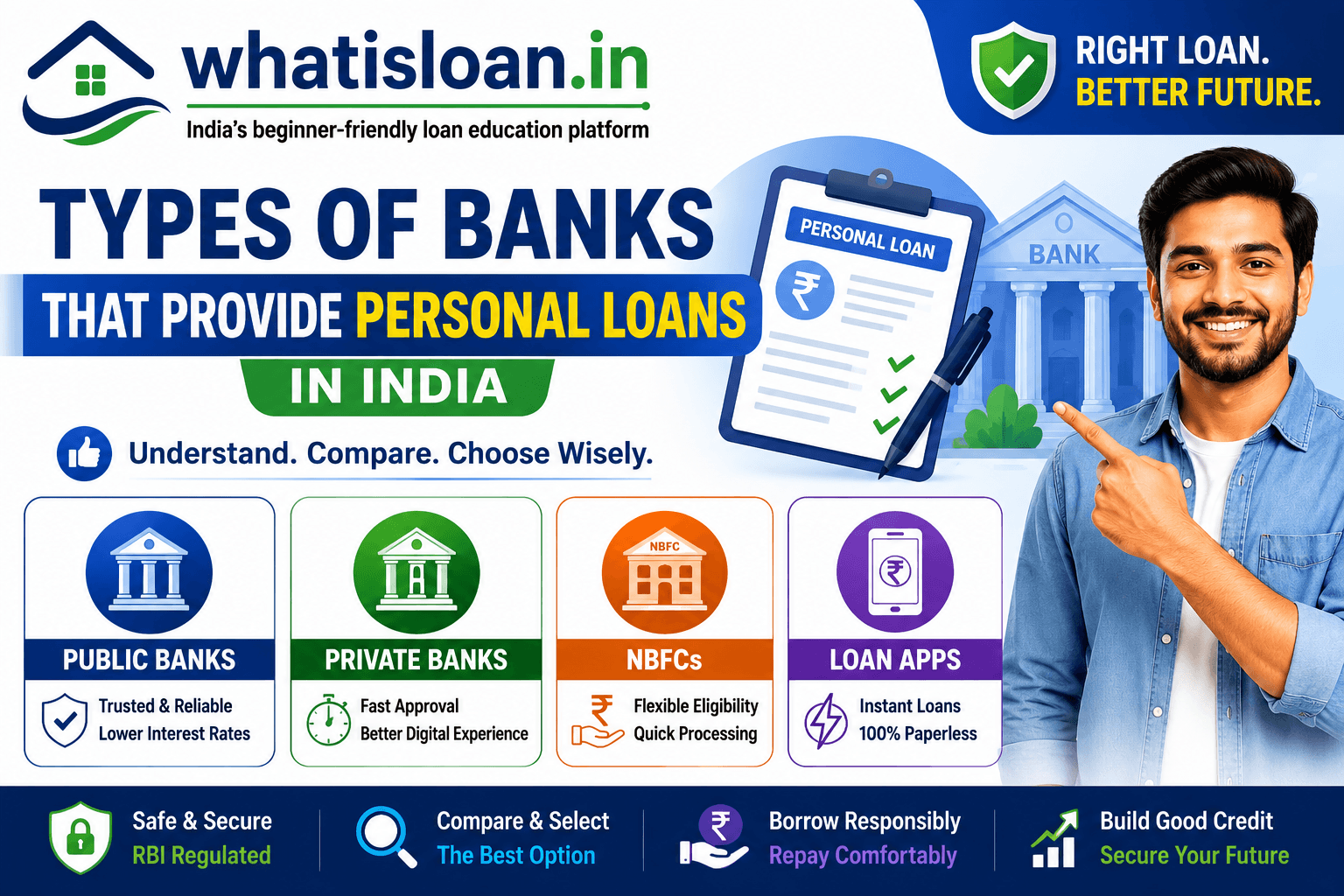

The process begins when you apply for a home loan with a bank or NBFC.

You need to submit:

- Personal details

- Income proof

- Employment details

- Property information

Many lenders now offer online home loan applications for faster processing.

Property Verification

Unlike personal loans, lenders carefully verify the property before approving the loan.

They check:

- Property ownership

- Legal approvals

- Market value

- Construction status

This helps reduce risk for the lender.

Credit Score and Eligibility Check

The lender evaluates your:

- Credit score

- Monthly income

- Existing debts

- Job stability

- Repayment history

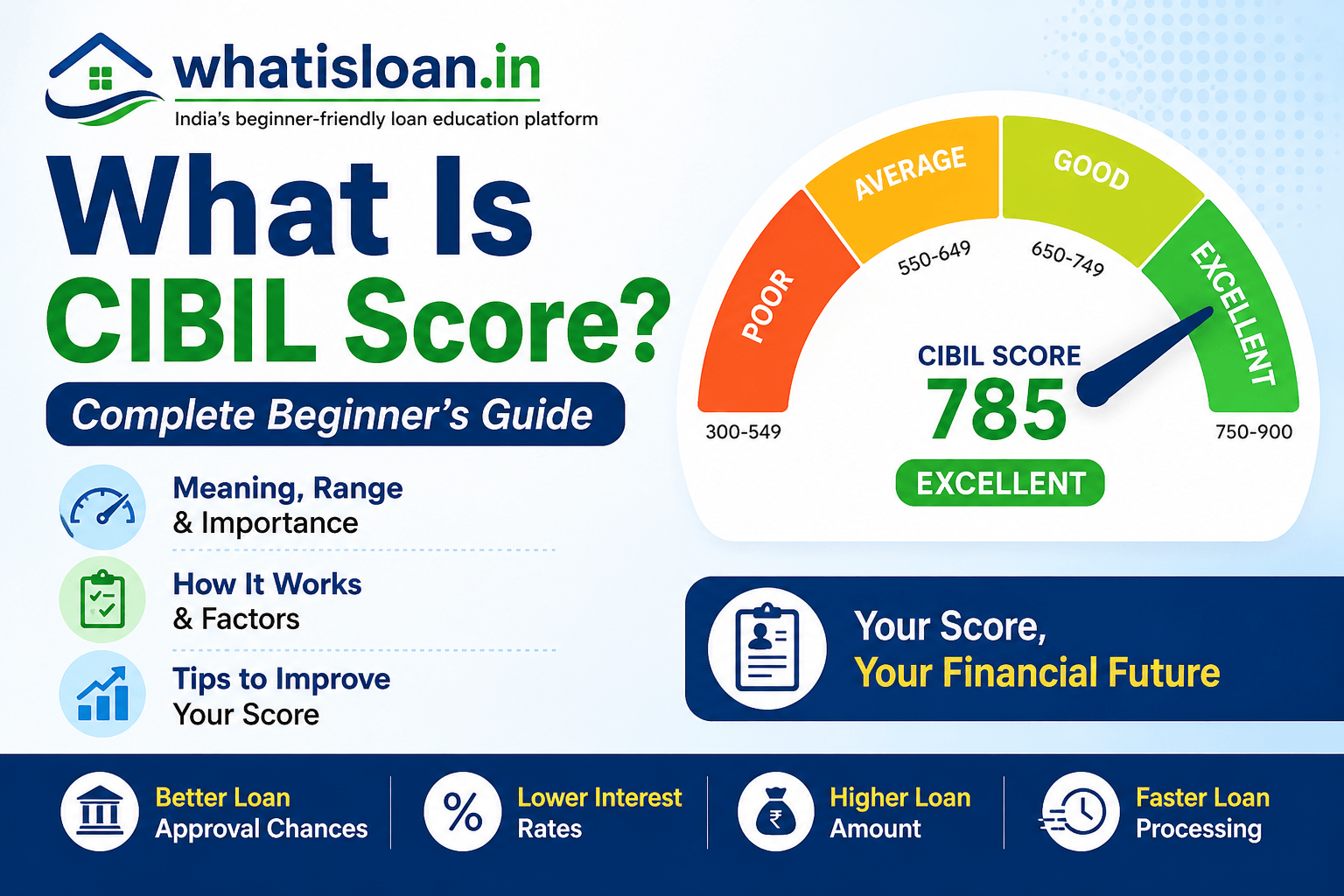

A higher CIBIL score increases the chances of approval and may help you secure lower interest rates.

Most lenders prefer a credit score of 750 or above for home loans.

Loan Approval and Sanction Letter

If your application is approved, the lender issues a sanction letter containing:

- Loan amount

- Interest rate

- Loan tenure

- EMI amount

- Terms and conditions

You should read the sanction letter carefully before accepting it.

Loan Disbursement Process

After property verification and document checks, the lender disburses the loan amount.

The money may be:

- Paid directly to the seller

- Released in stages for under-construction properties

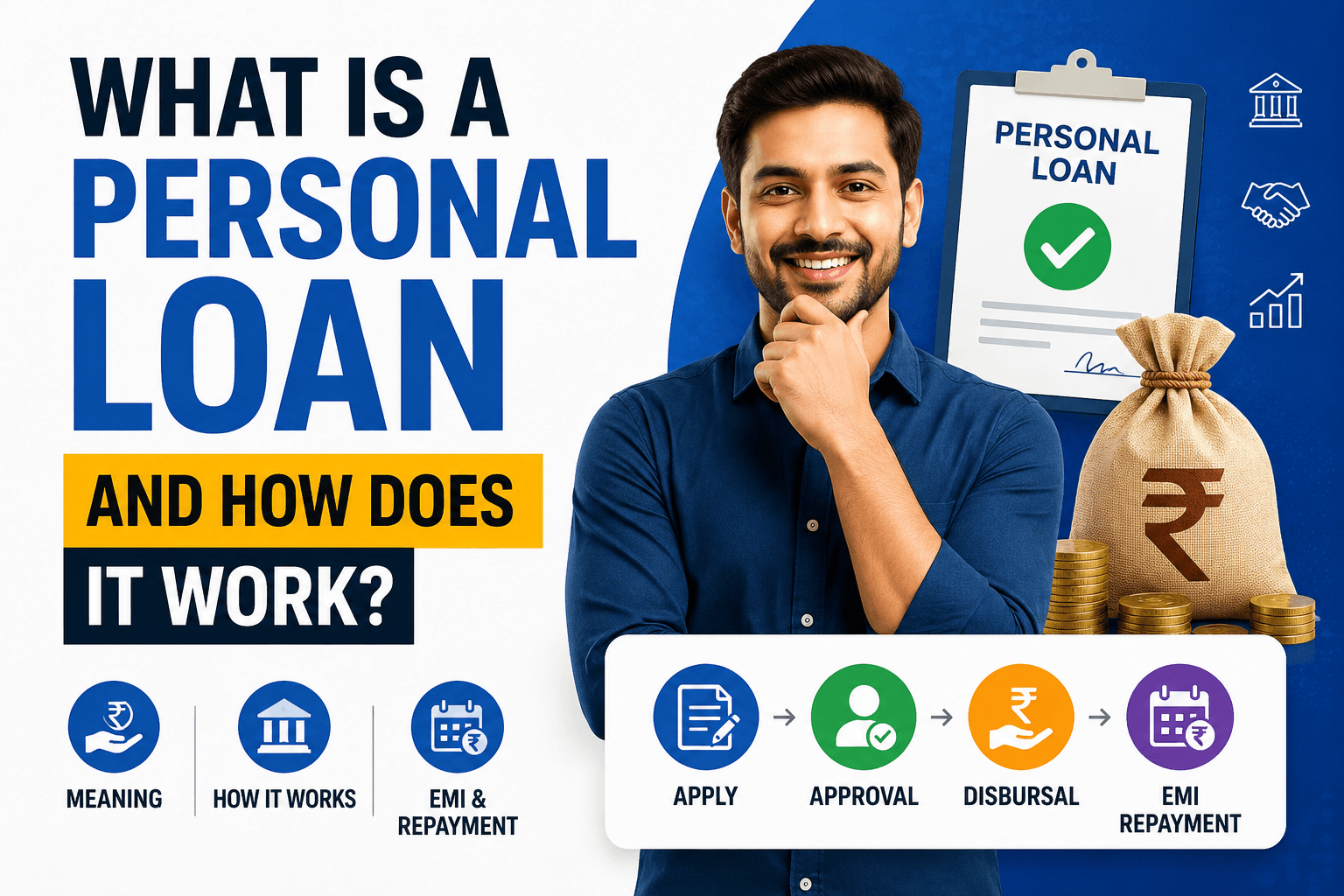

EMI Repayment Process

You repay the loan through monthly EMIs.

Each EMI contains:

- Principal amount

- Interest amount

The EMI amount depends on:

- Loan amount

- Interest rate

- Repayment tenure

Longer tenure reduces EMI but increases overall interest paid.

Types of Home Loans in India

Different types of home loans are available based on borrower needs.

Home Purchase Loan

Used to buy a ready-to-move or resale property.

Home Construction Loan

Designed for individuals constructing a house on owned land.

Home Renovation Loan

Used for repairing, upgrading, or renovating an existing home.

Plot Loan

Offered for purchasing residential plots or land.

Home Extension Loan

Useful when adding extra rooms or expanding the property.

Balance Transfer Home Loan

Allows borrowers to transfer an existing home loan to another lender offering lower interest rates.

PMAY Home Loan

Under the Pradhan Mantri Awas Yojana (PMAY), eligible borrowers may receive interest subsidies for affordable housing.

Key Features of a Home Loan

Some important features of home loans include:

- Long repayment tenure

- Lower interest rates

- High loan amount eligibility

- Property acts as collateral

- Tax-saving benefits

- EMI-based repayment

- Available for salaried and self-employed borrowers

Home Loan Eligibility Criteria

Eligibility varies by lender, but common requirements include:

| Criteria | Typical Requirement |

|---|---|

| Age | 21 to 65 years |

| Employment Type | Salaried or self-employed |

| Income Stability | Regular monthly income |

| Credit Score | Usually 750+ preferred |

| Work Experience | Stable employment/business |

| Property Status | Legally approved property |

Lenders may also consider your debt-to-income ratio before approving the loan.

Documents Required for Home Loan

You must submit various documents during the application process.

Identity and Address Proof

- Aadhaar card

- PAN card

- Passport

- Voter ID

Income Proof

Salaried Applicants

- Salary slips

- Form 16

- Bank statements

Self-Employed Applicants

- ITR documents

- Business proof

- GST returns

Property Documents

- Sale agreement

- Property title documents

- Approved building plan

- NOC documents

Employment Documents

- Employee ID

- Appointment letter

- Business registration proof

| Document | Purpose |

|---|---|

| Identity Proof | Verify applicant identity |

| Income Proof | Assess repayment capacity |

| Property Documents | Verify legal ownership |

| Bank Statements | Review financial stability |

Home Loan Interest Rates in India

Home loan interest rates vary based on:

- Lender policies

- Market conditions

- Borrower profile

In India, home loan interest rates generally range between 8% and 11% per annum.

Factors Affecting Interest Rates

Several factors influence your home loan interest rate:

- Credit score

- Monthly income

- Existing debts

- Loan amount

- Property value

- Employment profile

Borrowers with strong credit profiles usually receive better interest rates.

Processing Fees and Other Charges

Apart from interest rates, lenders may charge:

- Processing fees

- Legal verification charges

- Technical inspection fees

- Foreclosure charges

- Late payment penalties

Always check the complete loan cost before applying.

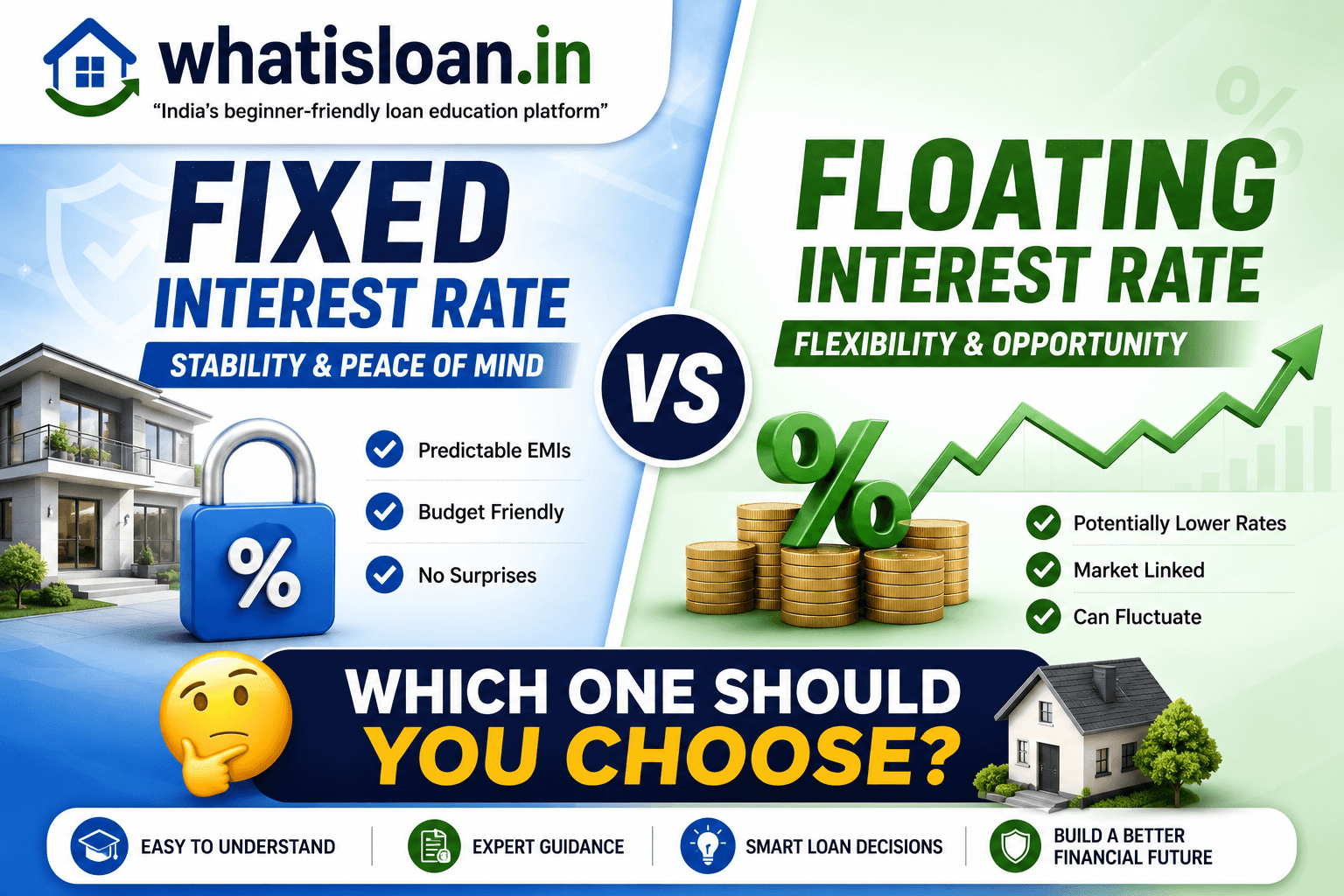

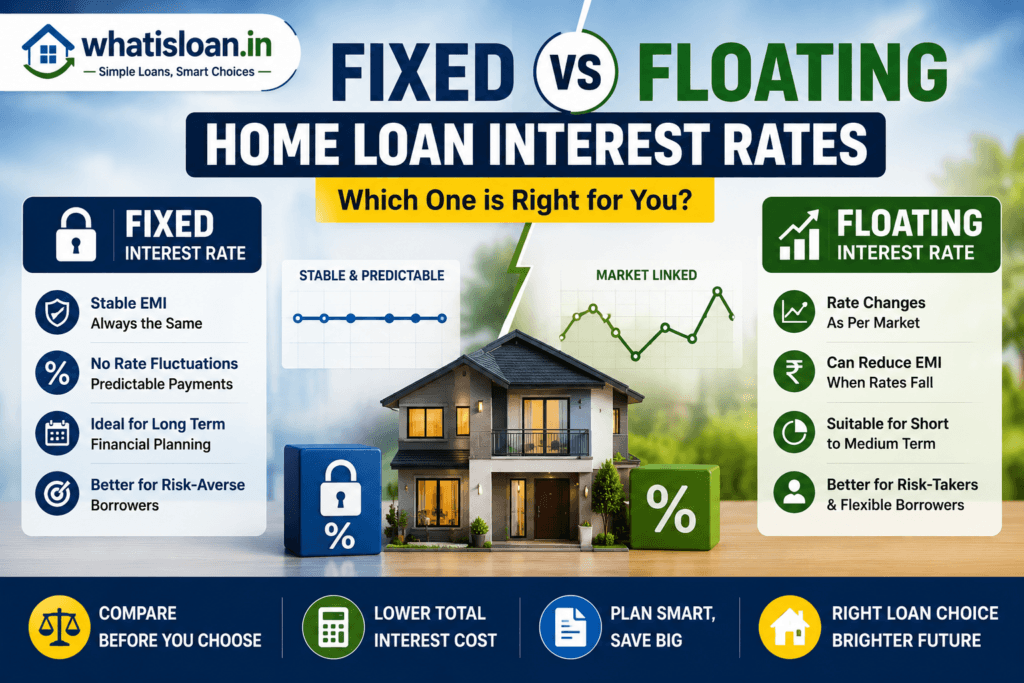

Fixed vs Floating Home Loan Interest Rates

| Feature | Fixed Interest Rate | Floating Interest Rate |

|---|---|---|

| EMI Stability | EMI remains stable | EMI may change |

| Interest Changes | Usually fixed for certain period | Changes with market rates |

| Risk Level | Lower uncertainty | Higher market risk |

| Flexibility | Less flexible | More flexible |

| Suitable For | Stable budgeting | Long-term savings potential |

Floating rates are common in India because they may reduce interest burden if market rates decline.

What Is Home Loan EMI?

EMI stands for Equated Monthly Installment.

It is the fixed monthly amount you pay to repay the loan.

Each EMI includes:

- Principal repayment

- Interest payment

The EMI depends on:

- Loan amount

- Interest rate

- Loan tenure

Before taking a home loan, always calculate whether the EMI comfortably fits your monthly income and lifestyle expenses.

Using a home loan EMI calculator can help estimate monthly repayment accurately.

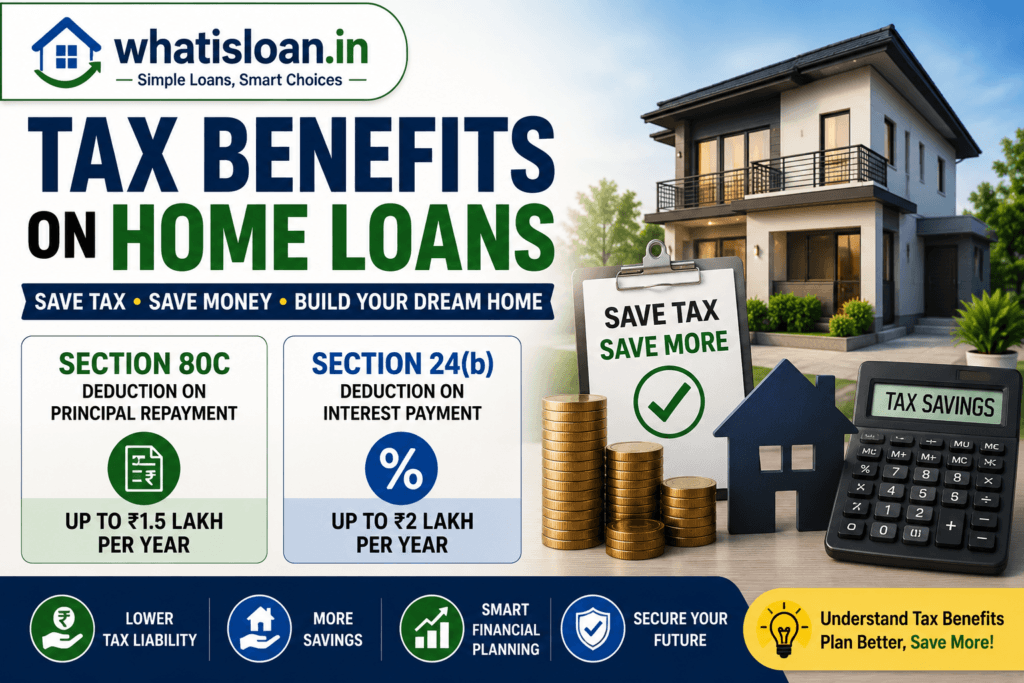

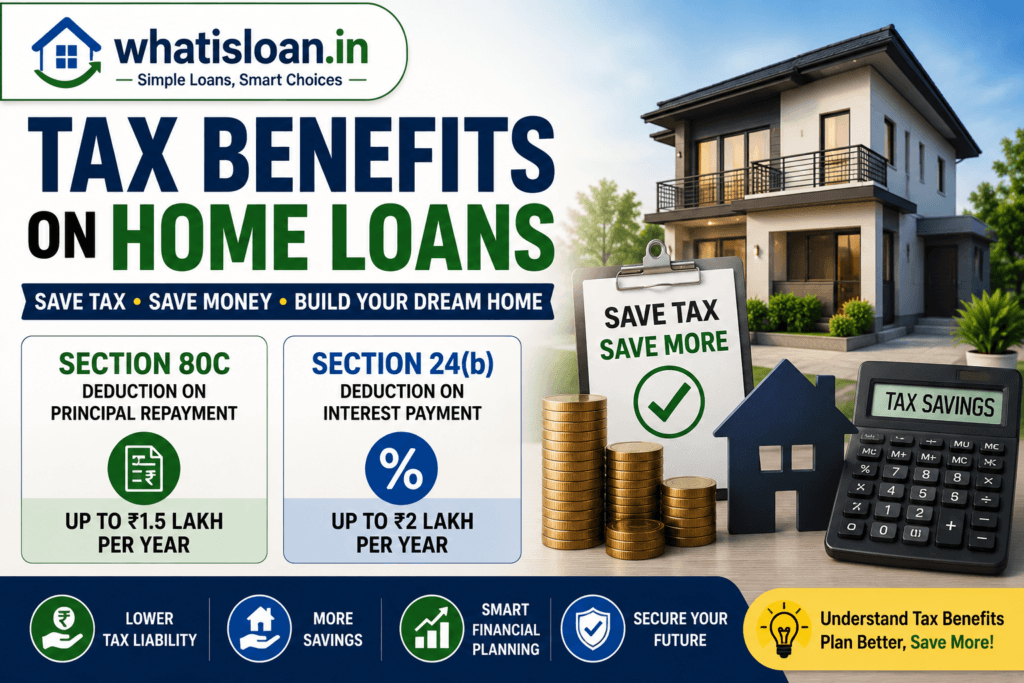

Tax Benefits on Home Loans

Home loans offer attractive tax benefits under Indian income tax laws.

Section 80C Benefits

You can claim deductions on principal repayment under Section 80C up to the applicable limit.

Section 24 Benefits

Interest paid on home loans may qualify for deductions under Section 24.

Tax Benefits for First-Time Buyers

Certain government schemes and tax provisions offer additional benefits for first-time home buyers.

Tax rules may change over time, so consult a tax advisor or official government resources for updated information.

Advantages of Home Loans

| Advantages | Explanation |

|---|---|

| Makes Home Ownership Possible | Helps buy property without full upfront payment |

| Lower Interest Rates | Cheaper than unsecured loans |

| Long Repayment Tenure | Reduces monthly EMI burden |

| Tax Benefits | Offers income tax deductions |

| High Loan Amounts | Suitable for expensive properties |

Disadvantages and Risks of Home Loans

| Disadvantages | Explanation |

|---|---|

| Long-Term Commitment | Repayment may continue for decades |

| Interest Burden | Total repayment may become significantly higher |

| Risk of Default | Property may be repossessed on non-payment |

| Additional Charges | Processing and legal fees increase costs |

| EMI Pressure | Missed payments affect credit score |

Borrow responsibly and avoid taking a loan beyond your repayment capacity.

Tips Before Applying for a Home Loan

Compare Multiple Lenders

Always compare:

- Interest rates

- Processing fees

- Loan tenure

- Customer service

before choosing a lender.

Maintain Good Credit Score

A strong credit score improves approval chances and helps secure lower interest rates.

Check EMI Affordability

Ensure the EMI fits comfortably within your monthly budget.

Understand Total Loan Cost

Focus not only on EMI but also:

- Total interest payable

- Hidden charges

- Processing fees

Read Loan Terms Carefully

Carefully review:

- Foreclosure rules

- Prepayment charges

- Penalty clauses

- Interest rate terms

before signing the agreement.

Common Reasons Home Loan Applications Get Rejected

Home loan applications may get rejected for several reasons.

Common reasons include:

- Low credit score

- Insufficient income

- Existing high debts

- Unstable employment

- Property legal issues

- Incorrect documentation

Improving your financial profile can increase future approval chances.

Key Takeaways

- A home loan helps you buy, build, or renovate property.

- Home loans are secured loans where the property acts as collateral.

- Lenders evaluate income, credit score, and repayment ability before approval.

- EMIs include both principal and interest repayment.

- Home loans offer tax benefits under Indian tax laws.

- Responsible borrowing and EMI planning are important.

FAQ Section

What is a home loan in simple words?

A home loan is money borrowed from a bank or lender to buy or build a house, which is repaid through monthly EMIs over a fixed period.

How does a home loan work?

The lender provides money for property purchase, and the borrower repays it with interest through monthly installments.

What is the minimum salary for a home loan?

The minimum salary requirement varies by lender, city, and loan amount.

Is a home loan secured or unsecured?

A home loan is a secured loan because the property acts as collateral.

What CIBIL score is required for a home loan?

Most lenders prefer a CIBIL score of 750 or above for home loan approval.

Can I repay a home loan early?

Yes, many lenders allow prepayment or foreclosure, although some conditions may apply.

What happens if I miss home loan EMI payments?

Missed EMI payments may result in penalties, legal action, and negative impact on your credit score.

Conclusion

A home loan can make home ownership possible without requiring the full property amount upfront. It is one of the most common and affordable ways to purchase a house in India. However, since home loans involve long-term financial commitments, understanding the loan process, EMI structure, interest rates, and repayment responsibilities is very important.

Before applying, compare multiple lenders, calculate your EMI carefully, and borrow only what you can comfortably repay. Responsible financial planning can help you manage your home loan efficiently while protecting your long-term financial stability.

Disclaimer

Home loan eligibility, interest rates, repayment terms, and tax benefits vary by lender and borrower profile. Interest rates and government policies may change over time. Always verify the latest information directly with banks, NBFCs, or official government sources before making financial decisions.