Unexpected expenses can come anytime. Whether you’ve to have cash for any medical emergency, marriage, minor renovation of your house, holiday or debt repayment. In such scenarios, most people in India opt for a personal loan as it helps you access funds instantly without needing any collateral.

But what is a personal loan, and how does it actually work?

If you are first-time borrower, dealing with personal loans can be difficult in the initial time. Term like EMI, interest rate, credit score, processing fee may sound difficult. The good news is that personal loans are actually simple once you understand the basics.

In this article, you will learn what is a personal loan, how does it works, eligibility criteria, interest rates, repayment process, advantages, disadvantages, and all important things you should know before applying for it.

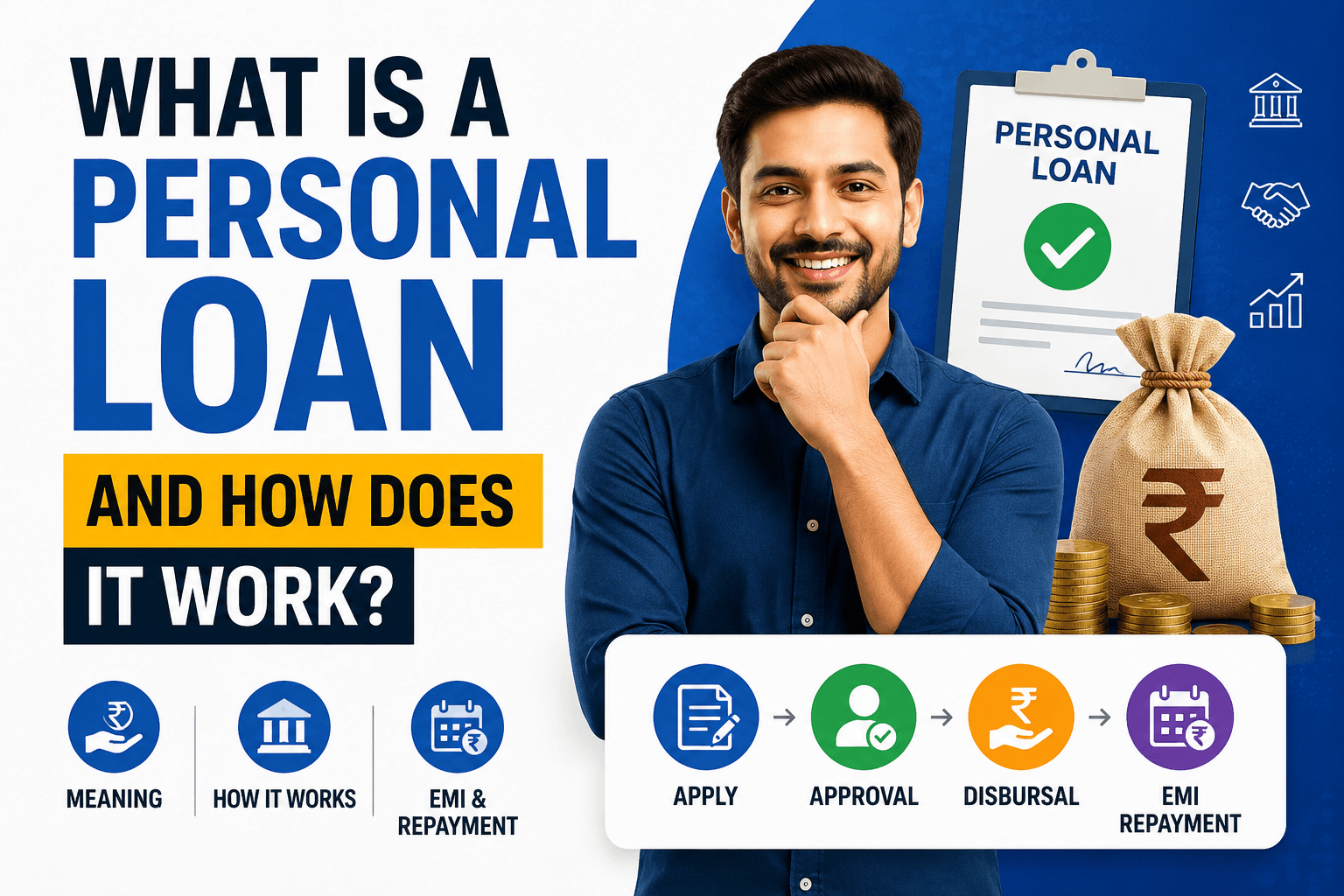

What Is a Personal Loan?

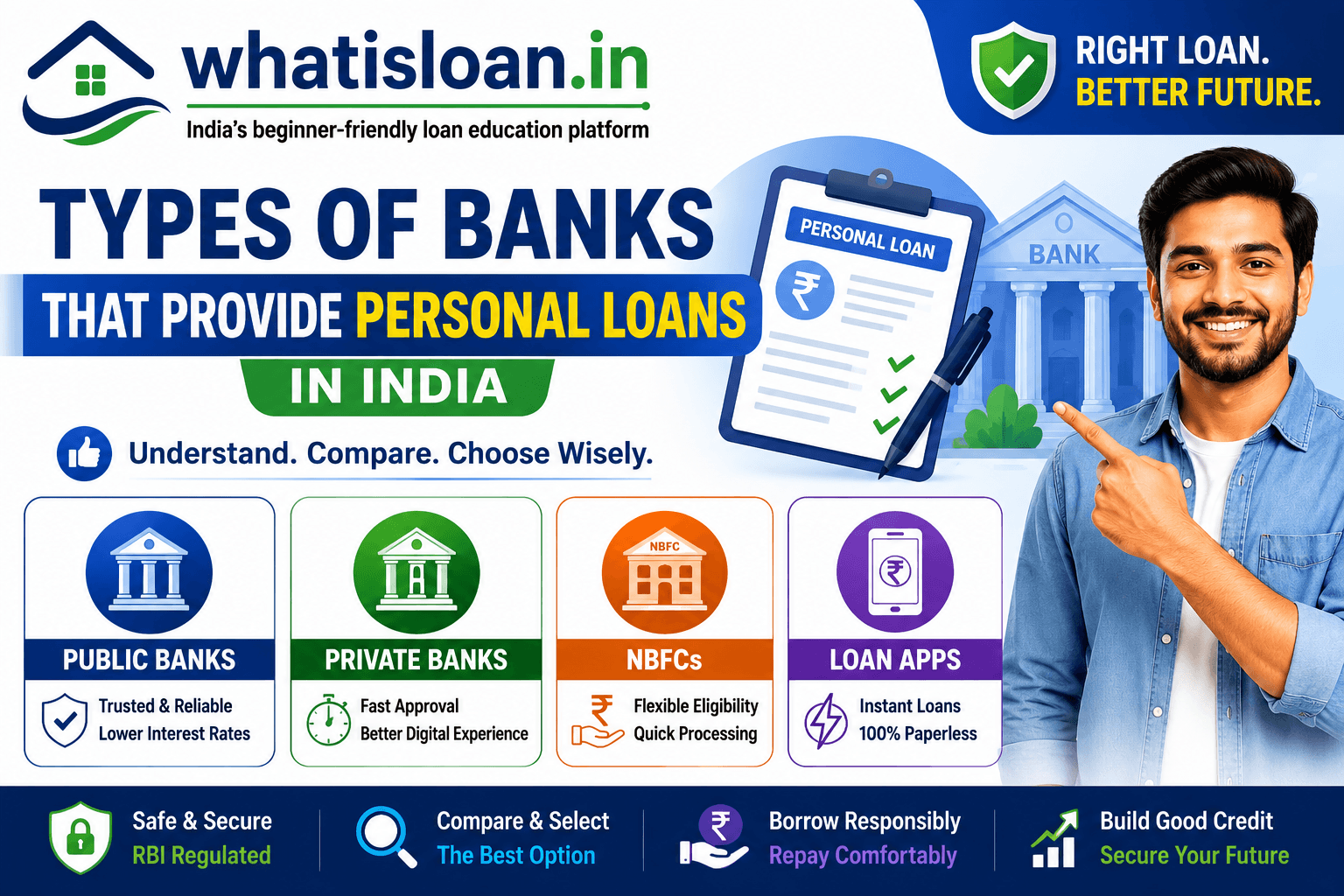

A personal loan is a type of unsecured loan that allows you to borrow money from a bank, NBFC, or digital lender without providing any collateral such as gold, property, or fixed deposits.

In simple words, the lender gives you a fixed amount of money, and you repay it in monthly installments called EMIs over a fixed period.

Since personal loans are unsecured, lenders mainly check your:

- Income

- Credit score

- Employment stability

- Repayment history

before approving your application.

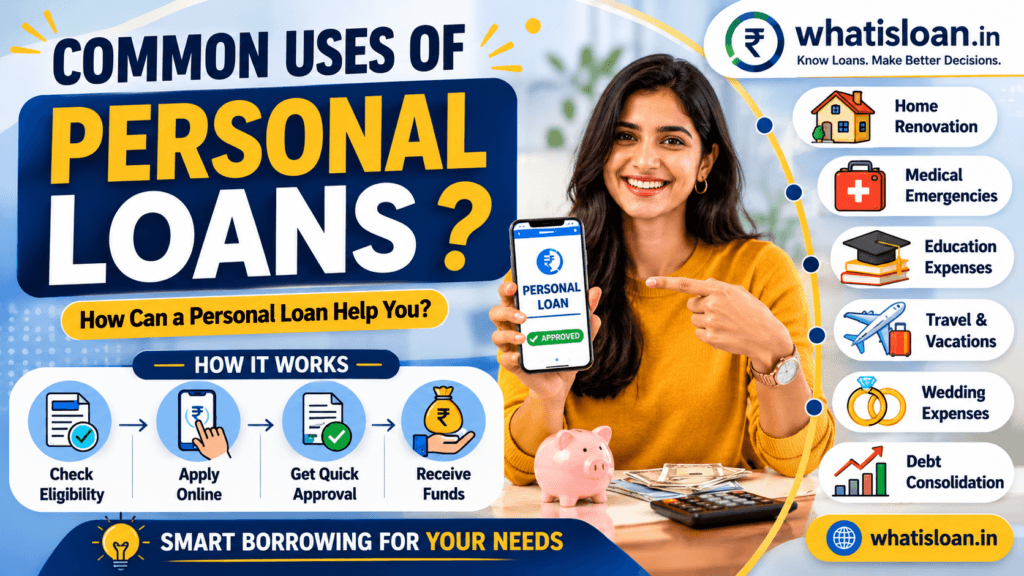

Personal loans are popular because you can use them for almost any legal purpose, including:

- Medical emergencies

- Weddings

- Travel

- Education expenses

- Home renovation

- Debt consolidation

Unlike home loans or car loans, there are usually no restrictions on how you use the money.

How Does a Personal Loan Work?

Understanding how a personal loan works is important before borrowing money.

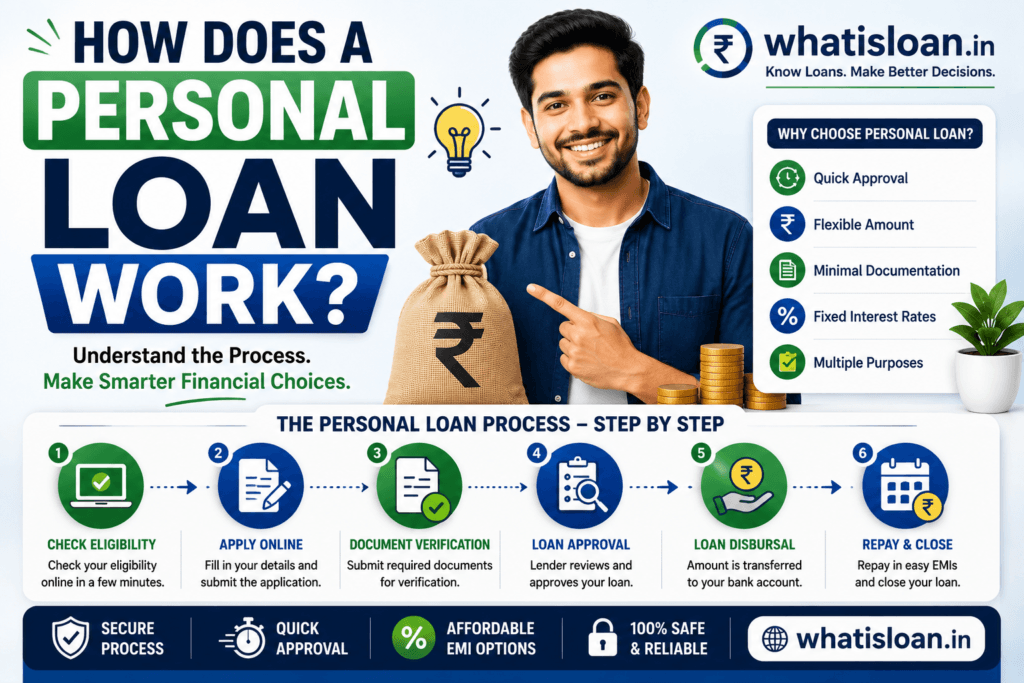

Loan Application Process

You can apply for a personal loan either online or offline.

Most banks and NBFCs now offer fully digital applications where you can:

- Fill out an application form

- Upload documents

- Complete KYC verification

- Check eligibility instantly

The lender then reviews your financial profile.

Credit Score and Eligibility Check

Lenders check several factors before approving a loan.

These include:

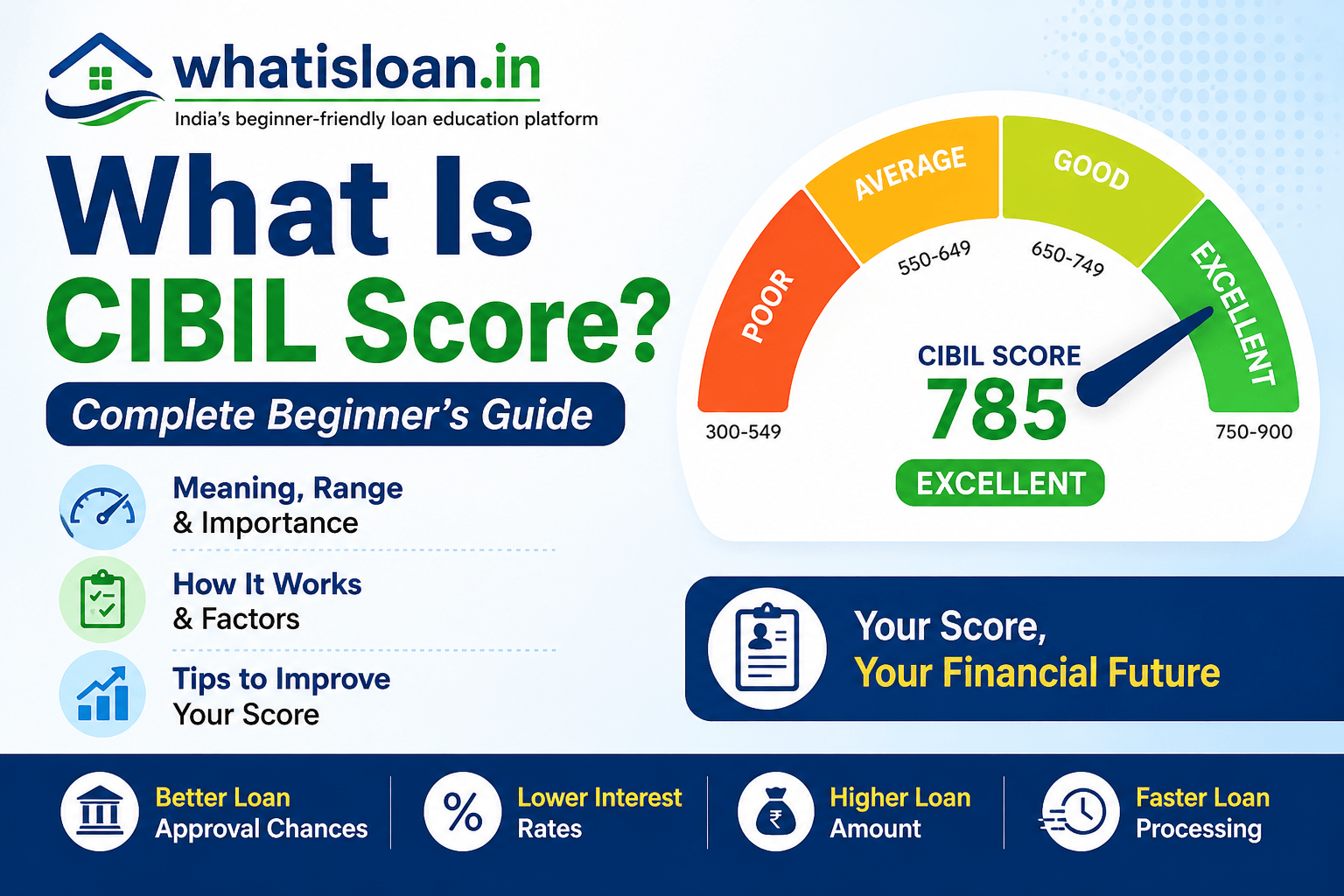

- Your CIBIL score

- Monthly income

- Existing loan obligations

- Employment type

- Job stability

A higher credit score mean higer chances of approval of your personal loan and may help you get a lower interest rate.

In India, most lenders prefer a CIBIL score of 700 or above for personal loans.

Loan Approval and Disbursement

If your application is approved, the lender sanctions the loan amount and transfers the money directly to your bank account.

Some instant personal loan apps disburse funds within a few hours, while traditional banks may take 1 to 3 working days.

EMI Repayment Process

After the loan amount is disbursed, you repay the loan through monthly EMIs.

An EMI includes:

- Principal amount

- Interest amount

The EMI is automatically deducted from your bank account through auto-debit or ECS.

The repayment tenure usually ranges from 12 months to 5 years.

What Happens After Loan Repayment?

Once you repay all EMIs successfully, the lender closes the loan account.

Timely repayment can improve your credit score and help you qualify for better and higher loans in the future.

Common Uses of Personal Loans

Personal loans are flexible and can be used for many purposes.

Medical Emergencies

Unexpected hospital bills can create financial pressure. Personal loans help cover urgent medical expenses quickly.

Wedding Expenses

Many people use personal loans to manage wedding costs such as venue booking, catering, decorations, and jewelry.

Home Renovation

You can use a personal loan to renovate your kitchen, repaint your home, or buy furniture and appliances.

Travel Expenses

Some borrowers use travel loans for vacations, international trips, or honeymoon planning.

Debt Consolidation

If you have multiple high-interest debts, a personal loan may help combine them into one manageable EMI.

Types of Personal Loans in India

Salaried Personal Loan

Designed for salaried employees with stable monthly income.

Self-Employed Personal Loan

Suitable for business owners, freelancers, and self-employed professionals.

Instant Personal Loan

Digital lenders and apps provide quick approvals and fast disbursal through online verification.

Balance Transfer Loan

Allows borrowers to transfer an existing personal loan to another lender offering lower interest rates.

Top-Up Personal Loan

Existing customers with good repayment history may get additional loan amounts over their current loan.

Key Features of a Personal Loan

Some important features of personal loans include:

- No collateral required

- Quick approval process

- Flexible loan usage

- Fixed repayment tenure

- Online application process

- EMI-based repayment

- Available for salaried and self-employed borrowers

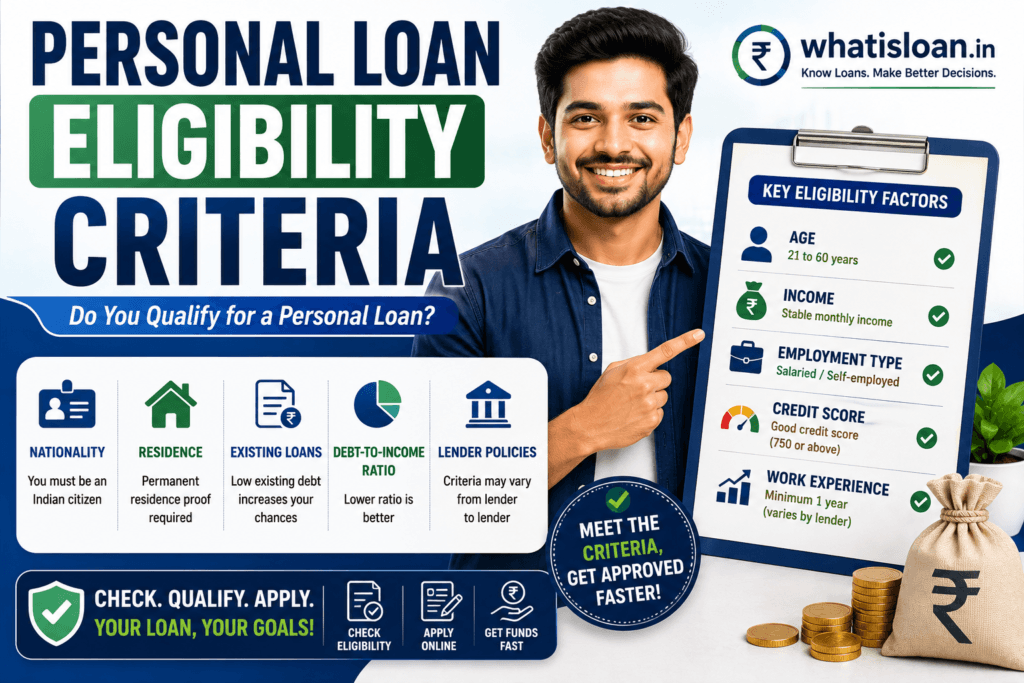

Personal Loan Eligibility Criteria

Eligibility rules vary by lender, but most banks and NBFCs follow common requirements.

| Criteria | Typical Requirement |

|---|---|

| Age | 21 to 60 years |

| Employment | Salaried or self-employed |

| Monthly Income | Minimum income requirement |

| Credit Score | Usually 700+ preferred |

| Work Experience | Stable employment history |

| Residency | Indian resident |

Lenders may have different policies based on risk assessment.

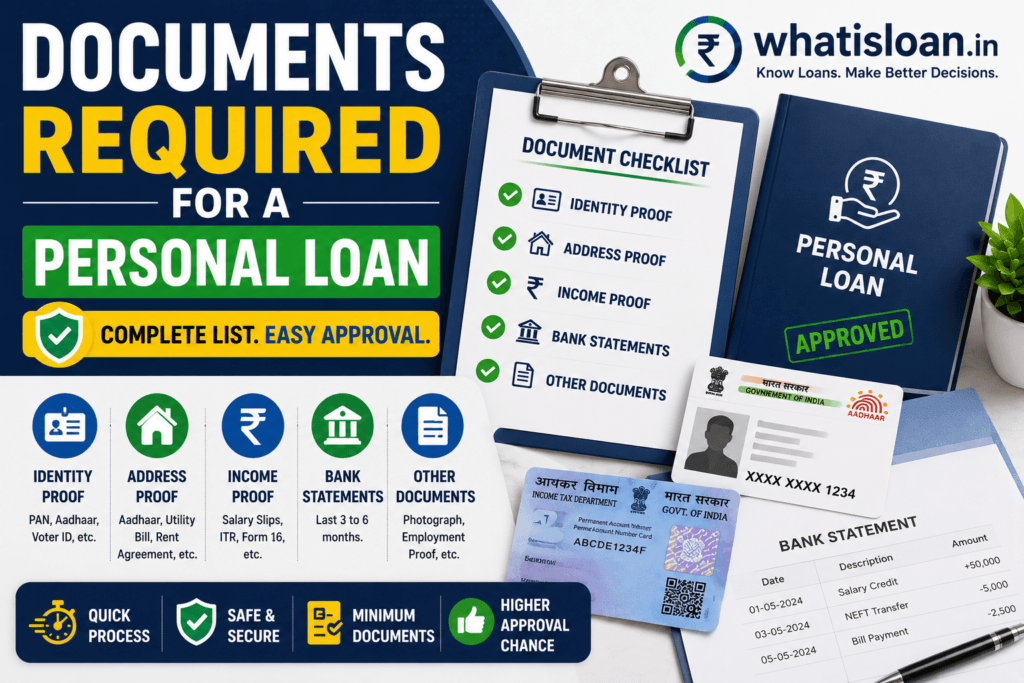

What documents are required for a personal loan?

Documents for Salaried Applicants

- PAN card

- Aadhaar card

- Salary slips

- Bank statements

- Employee ID proof

Documents for Self-Employed Applicants

- PAN card

- Aadhaar card

- ITR documents

- GST registration

- Business proof

- Bank statements

| Document Type | Purpose |

|---|---|

| Identity Proof | Verify applicant identity |

| Address Proof | Verify residence |

| Income Proof | Assess repayment capacity |

| Bank Statement | Review transaction history |

Personal Loan Interest Rates and Charges

Interest rates on personal loans vary depending on the lender and borrower profile.

In India, personal loan interest rates generally range between 10% and 24% per annum.

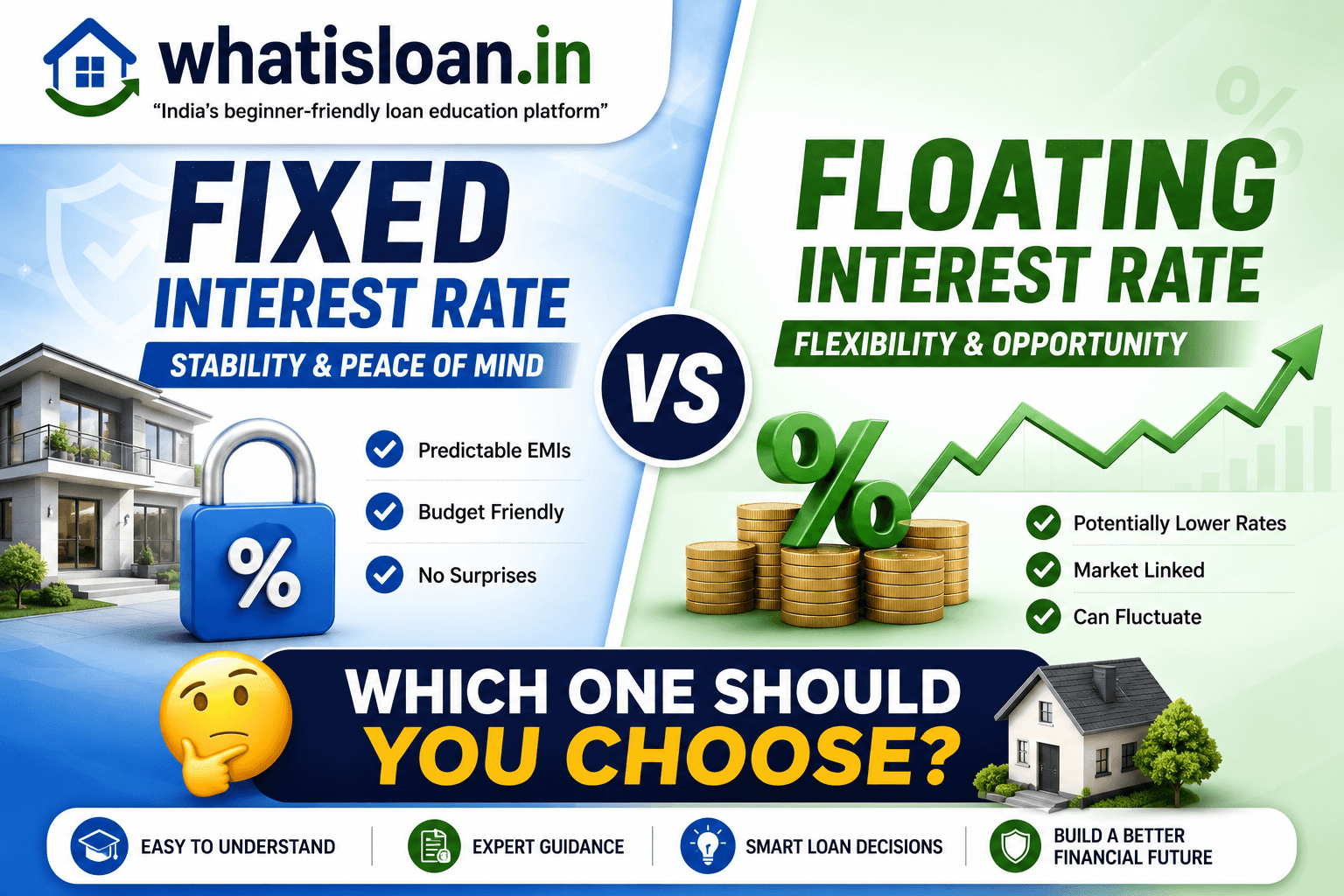

Fixed vs Floating Interest Rates

Fixed Interest Rate

Your EMI remains constant during the loan tenure.

Floating Interest Rate

Interest rate may change based on market conditions.

Most personal loans in India come with fixed interest rates.

Processing Fees and Hidden Charges

Apart from interest rates, lenders may charge:

- Processing fees

- Late payment penalties

- Foreclosure charges

- Bounce charges

- GST on fees

Always read the loan agreement carefully before signing.

Factors That Affect Interest Rates

Several factors influence your interest rate:

- Credit score

- Income level

- Employer category

- Existing debts

- Loan amount

- Repayment history

Borrowers with strong financial profiles usually receive better offers.

What is EMI in Personal Loan?

EMI stands for Equated Monthly Installment.

It is the fixed monthly amount you pay to repay your loan.

Each EMI contains:

- Principal repayment

- Interest payment

The EMI amount depends on:

- Loan amount

- Interest rate

- Loan tenure

Longer tenure reduces monthly EMI but increases total interest paid.

Shorter tenure increases EMI but reduces total interest cost.

Before taking a loan, always calculate whether the EMI comfortably fits your monthly budget.

Advantages of Personal Loans

Personal loans offer several benefits.

| Advantages | Explanation |

|---|---|

| Quick Approval | Faster processing compared to secured loans |

| No Collateral | No need to pledge assets |

| Flexible Usage | Can be used for multiple purposes |

| Easy Online Application | Fully digital process available |

| Fixed Repayment | Predictable EMI payments |

Disadvantages and Risks of Personal Loans

Personal loans also come with certain risks.

| Disadvantages | Explanation |

|---|---|

| Higher Interest Rates | Usually higher than secured loans |

| Penalty Charges | Late payment fees may apply |

| Credit Score Impact | Missed EMIs affect CIBIL score |

| Debt Burden | Excess borrowing can create stress |

| Processing Fees | Additional charges increase cost |

Borrow only what you can comfortably repay.

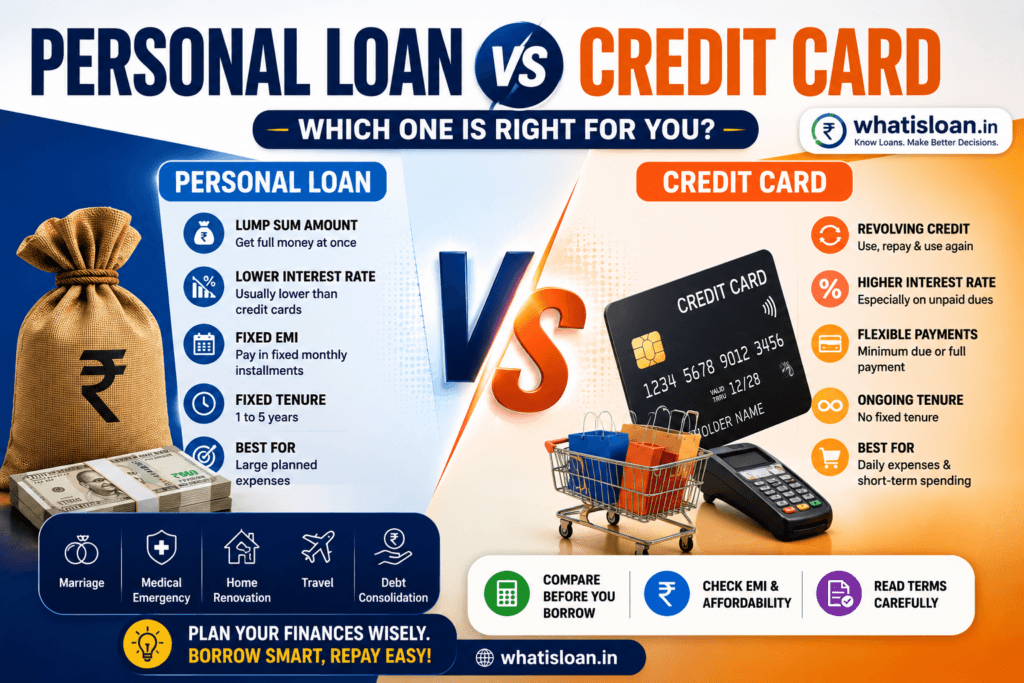

Personal Loan vs Credit Card

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Borrowing Type | You receive a fixed lump sum amount at once | You get a revolving credit limit that can be used multiple times |

| Interest Rate | Usually lower compared to credit cards | Usually higher, especially if dues are unpaid |

| Repayment Structure | Fixed monthly EMI over a set tenure | Flexible repayment with minimum due option |

| Loan Tenure | Fixed repayment period, usually 1 to 5 years | No fixed tenure if minimum dues are paid regularly |

| Usage Purpose | Best for large planned expenses like weddings, medical bills, or home renovation | Best for everyday spending, shopping, travel, and short-term purchases |

| Credit Limit | Depends on income, credit score, and lender eligibility | Pre-approved credit limit assigned by the card issuer |

| Processing Time | May take a few hours to a few days | Instant access once card is activated |

| Collateral Requirement | Usually unsecured and does not require collateral | No collateral required |

| EMI Availability | EMI starts immediately after loan disbursement | EMI option available on selected purchases |

| Impact of Missed Payments | Can affect credit score and lead to penalties | High interest charges and negative impact on credit score |

| Best Suitable For | Planned high-value expenses and debt consolidation | Short-term spending and emergency purchases |

Personal loans are generally better for planned large expenses, while credit cards are more suitable for short-term spending.

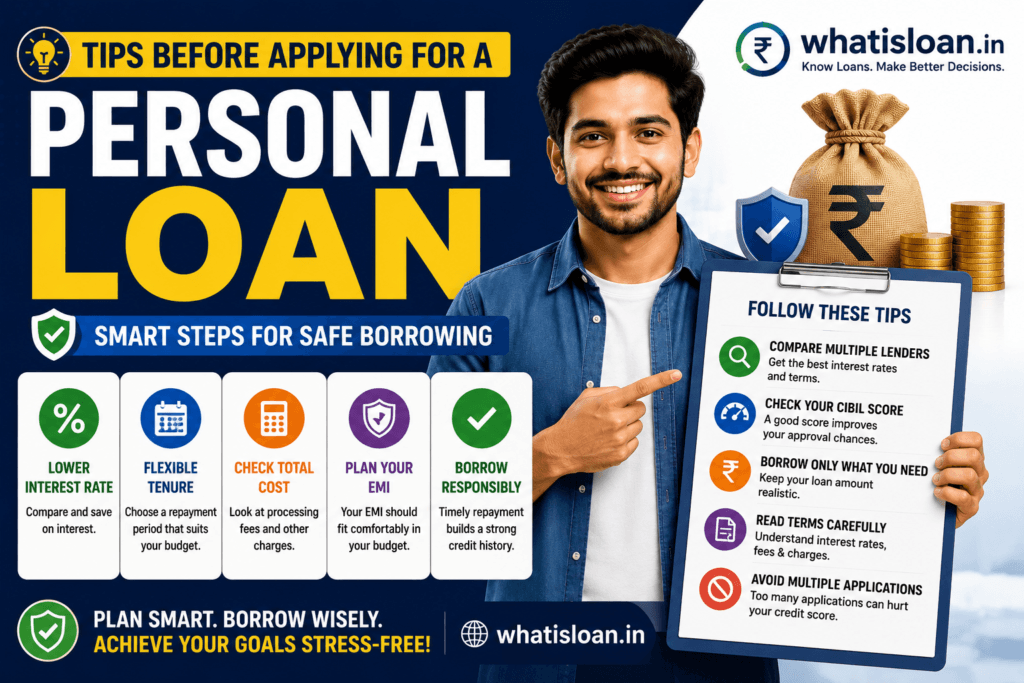

Tips Before Applying for a Personal Loan

Compare Multiple Lenders

Do not accept the first offer immediately. Compare:

- Interest rates

- Processing fees

- Repayment flexibility

- Foreclosure charges

Check Your CIBIL Score

A better credit score improves approval chances and helps secure lower interest rates.

Borrow Only What You Need

Avoid taking larger loans than necessary. Higher loan amounts increase repayment pressure.

Read Terms Carefully

Always review:

- Interest rates

- Hidden charges

- Penalty clauses

- Foreclosure rules

before signing the agreement.

Avoid Multiple Applications

Submitting applications to many lenders within a short time may affect your credit score.

Common Reasons Personal Loans Get Rejected

There are several reasons why your personal loan applications may be rejected.

Common causes include:

- Low credit score

- Insufficient income

- High existing debt

- Unstable job history

- Incorrect documents

- Frequent loan applications

Improving your financial profile can increase approval chances in the future.

Key Takeaways

- Personal loans are unsecured loans that do not require collateral.

- They are commonly used for emergencies, weddings, travel, and debt consolidation.

- Lenders check your income, employment, and credit score before approval.

- Personal loans are repaid through monthly EMIs.

- Interest rates and charges vary by lender.

- Responsible borrowing is important to avoid financial stress.

FAQ Section

What is a personal loan in simple words?

A personal loan is money borrowed from a bank or lender that you repay in monthly installments over a fixed period without providing collateral.

How does a personal loan work?

A lender approves a fixed loan amount based on your income and credit score. You repay the amount with interest through EMIs over a fixed tenure.

What CIBIL score is needed for a personal loan?

Most lenders prefer a CIBIL score of 700 or above, although some lenders may approve lower scores with higher interest rates.

Can I get a personal loan without collateral?

Yes, personal loans are unsecured loans, so collateral is usually not required.

How long does personal loan approval take?

Some lenders approve loans within a few hours, while others may take 1 to 3 working days.

What happens if I miss EMI payments?

Missing EMI payments may result in penalties and negatively affect your credit score.

Is a personal loan good or bad?

A personal loan can be useful for emergencies and planned expenses if borrowed responsibly and repaid on time.

Conclusion

A personal loan can be a useful financial tool when you need quick access to funds for emergencies or important expenses. Since these loans do not require collateral, they are easier to access compared to many secured loans. However, understanding how personal loans work is important before borrowing.

Always compare lenders carefully, check the total cost of borrowing, and ensure the EMI fits your monthly budget comfortably. Responsible borrowing and timely repayment not only help you avoid financial stress but also improve your credit profile over time.

Before applying, take time to evaluate your financial situation and choose a loan that matches your repayment capacity.

Disclaimer

Loan eligibility, interest rates, charges, and repayment terms vary by lender and borrower profile. Interest rates may change over time based on market conditions and lender policies. Always verify the latest details directly with banks, NBFCs, or official lender websites before applying for a personal loan.