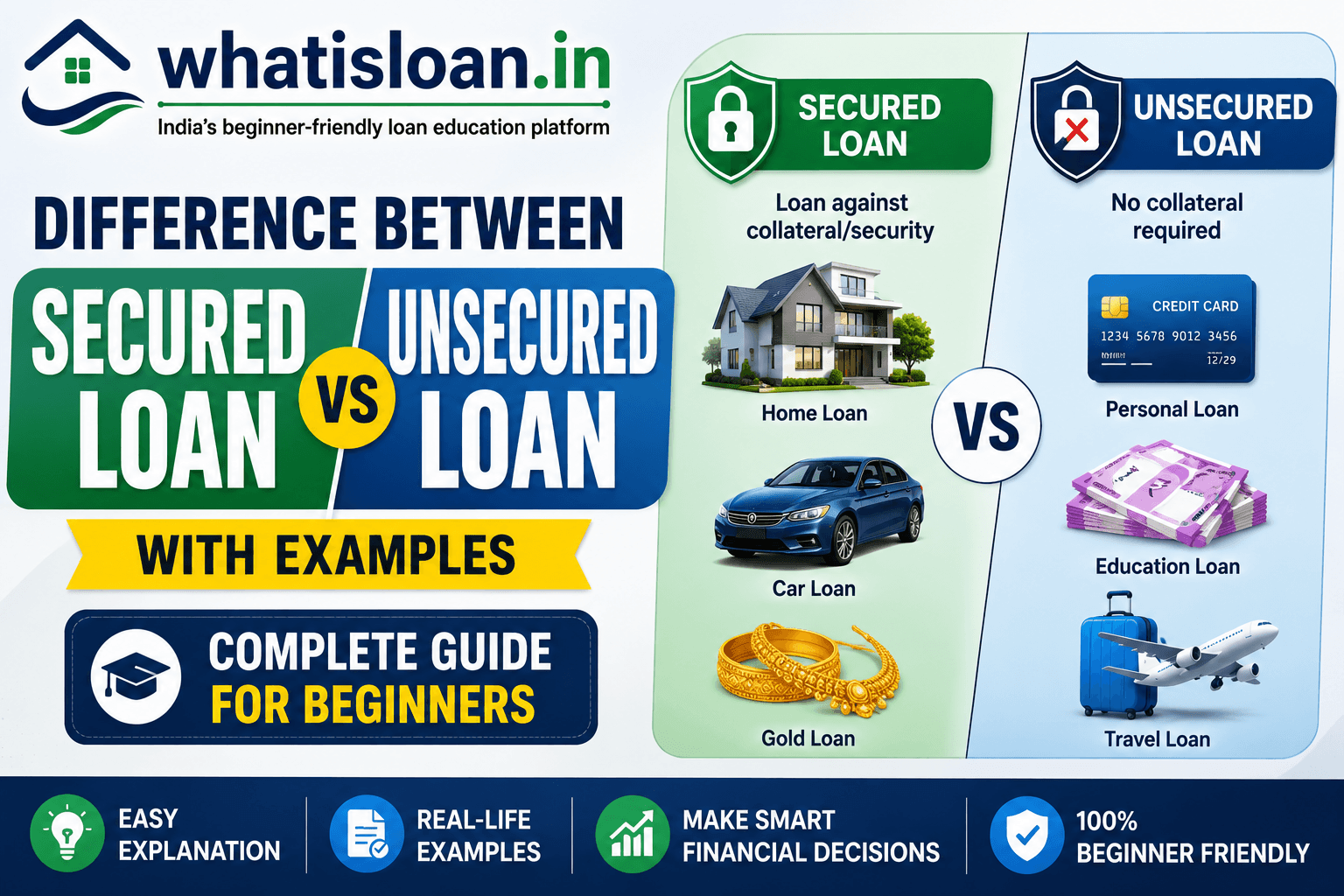

If you are planning to borrow money, understanding the difference between secured and unsecured loan with examples is important. While both types of loans help meet financial needs, they work differently. The biggest difference lies in collateral. Secured loans require an asset as security, whereas unsecured loans do not. Knowing these differences helps you choose the right loan based on your financial goals, repayment ability, and available assets.

What Is a Loan?

A loan is money borrowed from a bank, NBFC, or financial institution with an agreement to repay the amount along with interest over a specified period. Loans help individuals and businesses meet financial needs such as buying a home, purchasing a vehicle, funding education, or managing emergencies.

There are various types of loans available in India, including home loans, personal loans, car loans, education loans, and business loans. If you want to understand business financing in detail, read our guide on What Is a Business Loan?.

What Is a Secured Loan?

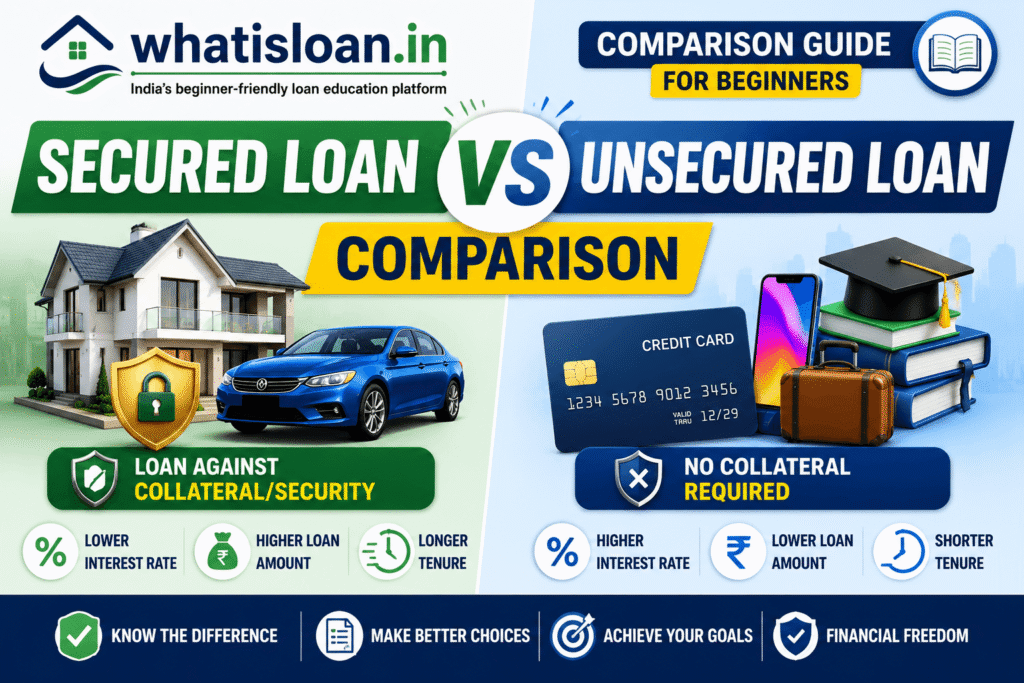

A secured loan is a loan backed by collateral. The borrower pledges an asset to the lender as security. If the borrower fails to repay the loan, the lender has the right to seize or sell the asset to recover the outstanding amount.

Collateral may include:

- House or property

- Gold ornaments

- Vehicle

- Fixed deposits

- Investments

Because secured loans involve lower risk for lenders, they often come with lower interest rates and larger loan amounts.

Examples of Secured Loans

Some common examples of secured loans include:

- Home Loan: The purchased property acts as collateral. Learn more in our guide on What Is a Home Loan?.

- Gold Loan: Borrowers pledge gold ornaments to receive funds quickly.

- Car Loan: The financed vehicle remains under the lender’s charge until repayment.

- Loan Against Property: Existing property is used as security.

- Loan Against Fixed Deposit: Banks provide loans against FDs at lower interest rates.

Many borrowers compare lenders before applying. Check out our list of the Best Banks for Home Loans in India.

What Is an Unsecured Loan?

An unsecured loan is a loan that does not require any collateral. Approval depends mainly on your income, employment history, credit score, and repayment capacity.

Since lenders face higher risk, unsecured loans generally have higher interest rates compared to secured loans.

Unsecured loans are ideal for borrowers who do not own valuable assets or require quick access to funds.

Examples of Unsecured Loans

Examples of unsecured loans include:

- Personal Loan

- Credit Card Loan

- Consumer Durable Loan

- Education Loan without collateral

- Short-term Business Loan

If you want to know more, read our detailed article on What Is a Personal Loan and How Does It Work?.

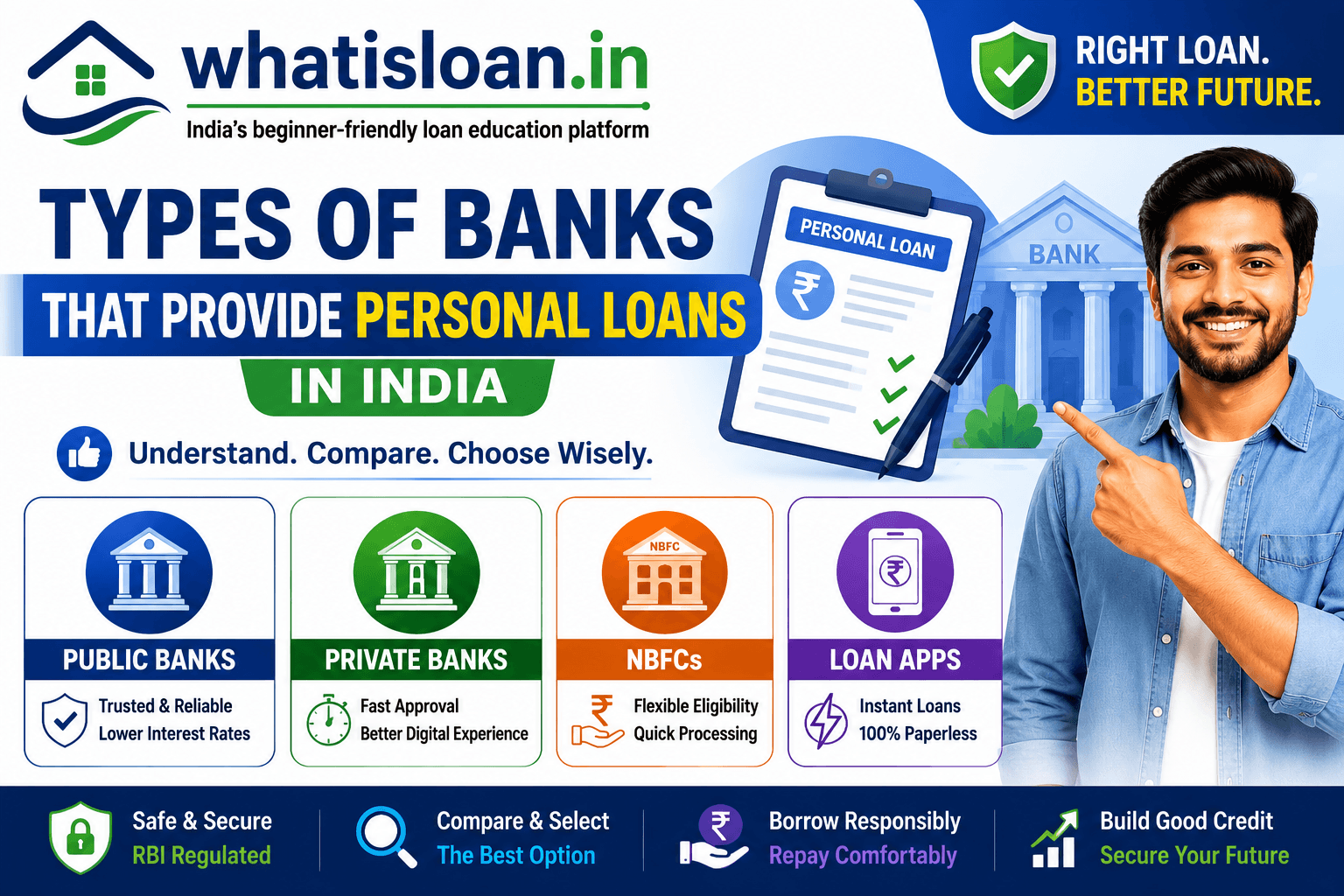

You can also explore Types of Banks That Provide Personal Loans in India.

Difference Between Secured and Unsecured Loan with Examples

The difference between secured and unsecured loan with examples mainly lies in collateral, risk, interest rates, and eligibility criteria.

For example, a home loan is a secured loan because the property acts as security. A personal loan is an unsecured loan because no asset is pledged.

Similarly, a gold loan is secured because gold ornaments serve as collateral, while a credit card loan is unsecured because approval depends on the borrower’s creditworthiness.

Secured Loan vs Unsecured Loan Comparison Table

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral | Required | Not Required |

| Interest Rate | Lower | Higher |

| Loan Amount | Higher | Lower |

| Approval Time | Moderate | Faster |

| Risk to Borrower | Asset may be seized | No asset risk |

| Credit Score Importance | Moderate | High |

| Repayment Tenure | Longer | Shorter |

| Examples | Home Loan, Gold Loan | Personal Loan, Credit Card Loan |

Advantages of Secured Loans

Secured loans offer several benefits:

- Lower interest rates

- Higher loan eligibility

- Longer repayment tenure

- Larger loan amounts

- Better chances of approval

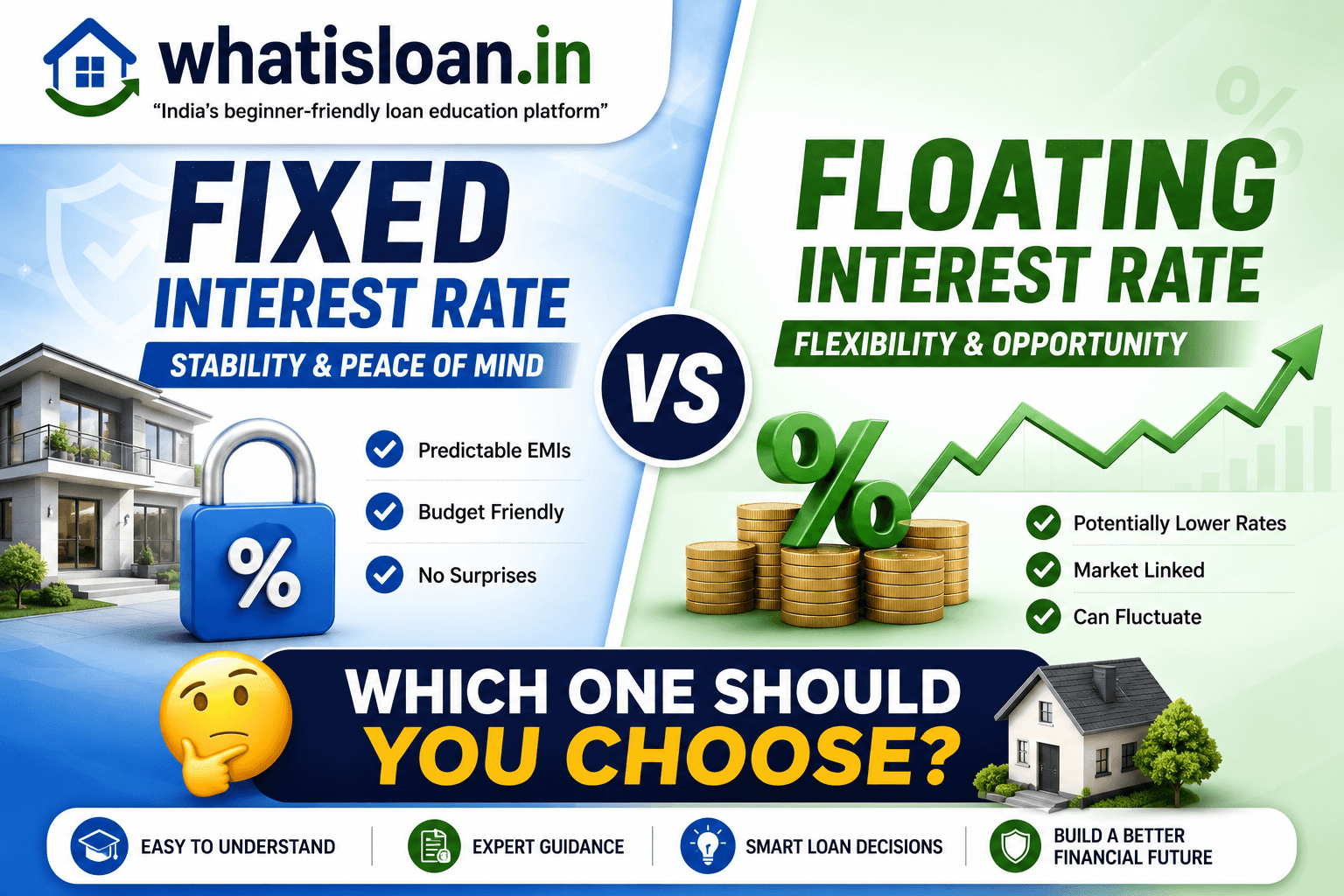

Borrowers often compare loan options and interest structures before applying. Learn more about Fixed vs Floating Interest Rate.

Disadvantages of Secured Loans

Secured loans also have certain drawbacks:

- Risk of losing the pledged asset

- Longer approval process

- Additional documentation requirements

- Asset valuation charges

Advantages of Unsecured Loans

Unsecured loans provide several advantages:

- No collateral required

- Quick approval process

- Minimal documentation

- Flexible use of funds

These features make personal loans popular for emergencies and short-term financial needs.

Disadvantages of Unsecured Loans

Some disadvantages include:

- Higher interest rates

- Lower borrowing limits

- Strict eligibility criteria

- Greater dependence on credit score

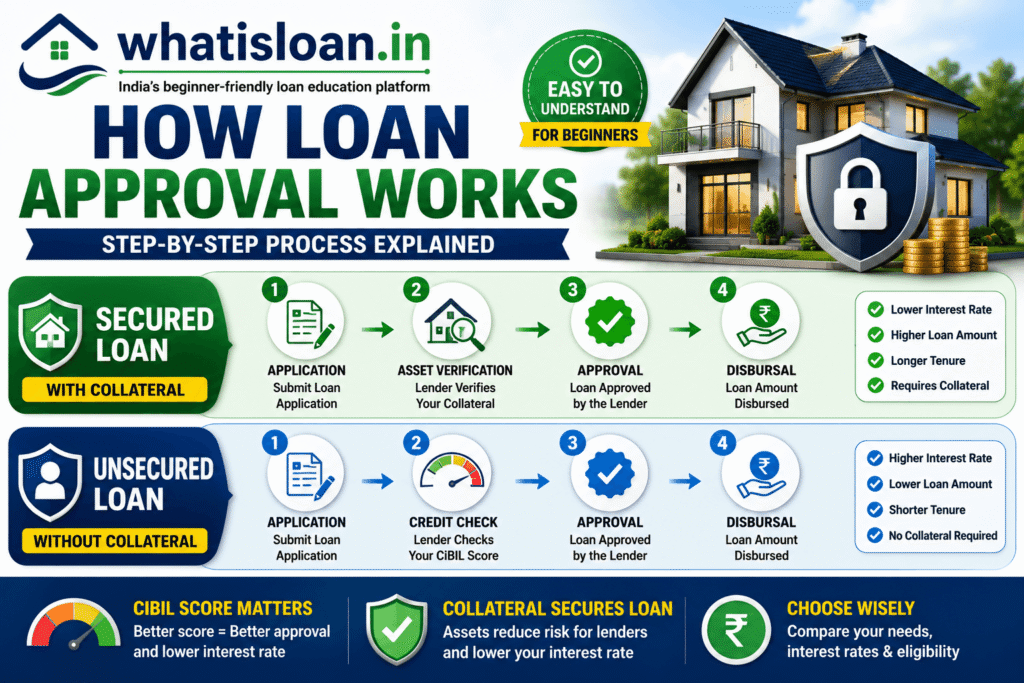

How Do Banks Decide Loan Eligibility?

Banks evaluate several factors before approving a loan:

- Income level

- Employment stability

- Existing loan obligations

- Age of the borrower

- Credit history

- CIBIL score

Lenders use these factors to assess the borrower’s repayment capacity and overall risk profile.

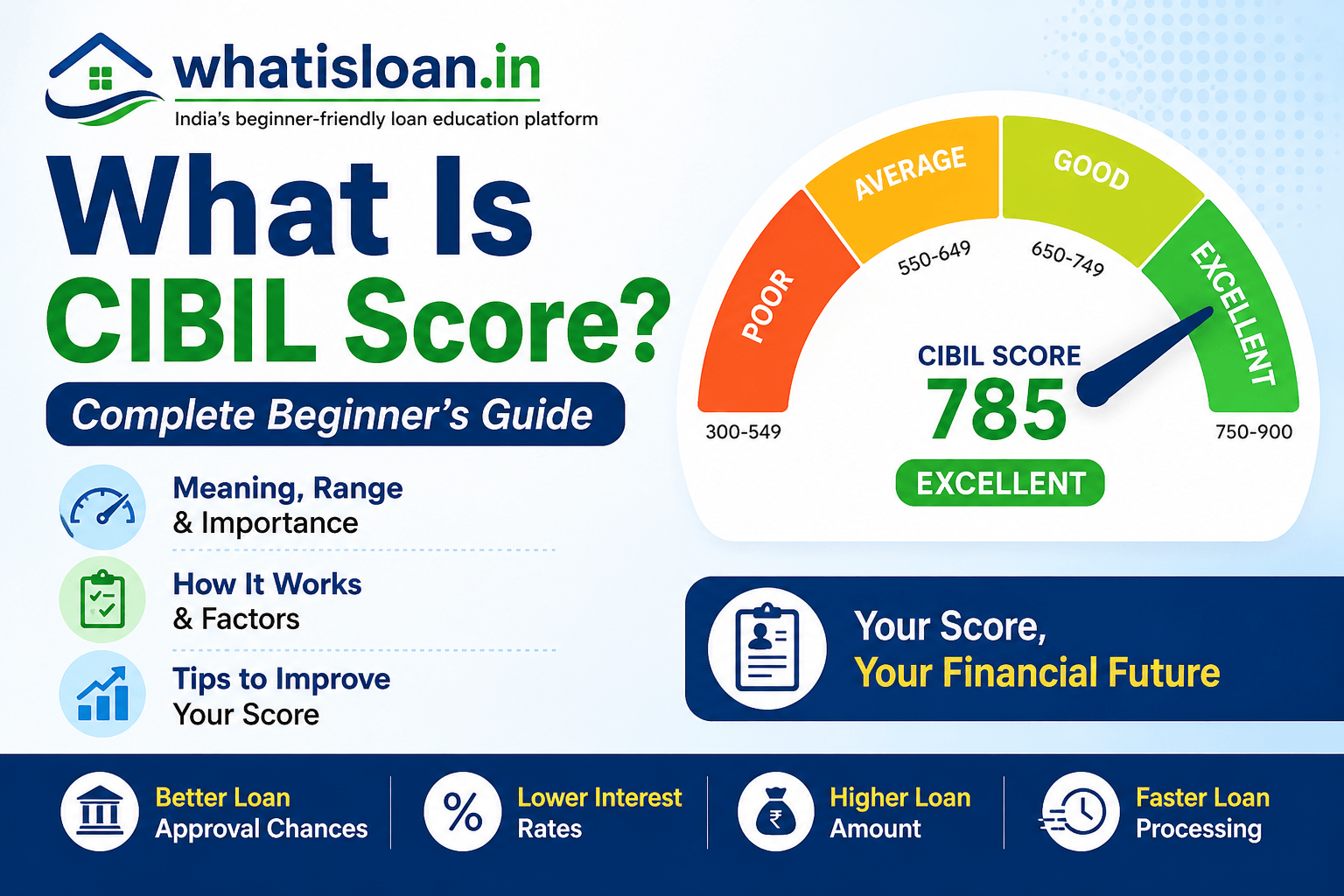

How Does CIBIL Score Affect Loans?

A CIBIL score plays an important role in loan approval. A higher score indicates responsible credit behavior and improves your chances of approval.

Generally:

- 750 and above: Excellent

- 700–749: Good

- Below 650: Difficult approval

Learn more in our guide on What Is CIBIL Score?.

Interest Rates in Secured vs Unsecured Loans

Interest rates differ significantly between secured and unsecured loans.

Typical ranges in India:

- Home Loan: 8% to 10%

- Gold Loan: 8% to 15%

- Personal Loan: 10% to 24%

- Credit Card Loan: 18% to 36%

Choosing between fixed and floating interest rates can significantly impact your EMIs and total repayment amount.

What Happens if You Default on a Loan?

Loan default has serious consequences.

For secured loans:

- The lender may seize collateral.

- Assets may be auctioned.

- Legal recovery actions may be initiated.

For unsecured loans:

- Penalties and late fees apply.

- Your credit score falls.

- Future borrowing becomes difficult.

Timely repayment helps maintain a healthy credit profile.

Which Loan Is Better for You?

A secured loan may be suitable if:

- You need a large amount.

- You own assets.

- You want lower interest rates.

An unsecured loan may be suitable if:

- You need funds quickly.

- You do not own collateral.

- You require a smaller loan amount.

The right choice depends on your financial goals, repayment ability, and risk tolerance.

Tips for Choosing the Right Loan

Before applying for a loan:

- Compare interest rates.

- Check processing fees.

- Review prepayment charges.

- Evaluate EMI affordability.

- Maintain a good CIBIL score.

- Borrow only what you need.

Careful planning helps reduce financial stress and improves repayment success.

Key Takeaways

- Secured loans require collateral.

- Unsecured loans do not require collateral.

- Secured loans offer lower interest rates.

- Unsecured loans provide faster approval.

- CIBIL score is especially important for unsecured loans.

- Home loans and gold loans are secured loans.

- Personal loans and credit card loans are unsecured loans.

Frequently Asked Questions (FAQs)

Is a home loan secured or unsecured?

A home loan is a secured loan because the property being purchased serves as collateral for the lender. When a bank or financial institution approves a home loan, it places a charge on the property until the borrower fully repays the loan. If the borrower fails to repay the EMIs for a prolonged period, the lender has the legal right to take possession of the property and sell it to recover outstanding dues. Since home loans are backed by collateral, lenders face lower risk and often offer lower interest rates and longer repayment tenures. Home loans in India usually have repayment periods of up to 30 years. Borrowers with a good credit profile and stable income may qualify for better interest rates and higher loan amounts.

Is a personal loan secured or unsecured?

A personal loan is generally an unsecured loan because borrowers are not required to pledge any asset or collateral. Banks and NBFCs approve personal loans based on factors such as income, employment history, repayment capacity, and CIBIL score. Since lenders do not have any security against the loan, they assume higher risk. As a result, personal loans often carry higher interest rates compared to secured loans such as home loans or gold loans. Personal loans are commonly used for medical emergencies, travel, weddings, home renovations, or debt consolidation. Maintaining a high credit score and stable income increases the chances of approval and may help borrowers obtain lower interest rates and better loan terms.

Which loan has lower interest rates?

Secured loans typically have lower interest rates than unsecured loans because they are backed by collateral. When borrowers pledge an asset such as property, gold, or a vehicle, lenders face less risk of financial loss. This reduced risk allows banks to offer lower interest rates and larger loan amounts. For example, home loans and gold loans often have interest rates ranging from 8% to 12%, while personal loans may have rates ranging from 10% to 24% or even higher. The exact interest rate depends on factors such as CIBIL score, income, loan tenure, and lender policies. Borrowers should compare fixed and floating interest rates before choosing a loan to reduce their overall borrowing costs.

Can I get a loan without collateral?

Yes, you can get a loan without collateral through unsecured loans. In these loans, borrowers are not required to pledge assets such as property, gold, or vehicles. Common examples include personal loans, credit card loans, and some education loans. Instead of collateral, lenders evaluate the applicant’s income, employment stability, credit history, and CIBIL score to determine eligibility. While unsecured loans provide quick access to funds and involve minimal paperwork, they usually come with higher interest rates because lenders bear greater risk. The approved loan amount may also be lower than secured loans. Maintaining a good credit score and stable repayment history improves the chances of approval and helps borrowers secure better loan terms.

Does CIBIL score matter for secured loans?

Yes, the CIBIL score matters for secured loans, although its importance is generally greater for unsecured loans. Lenders use the CIBIL score to assess a borrower’s creditworthiness and repayment behavior. A high credit score indicates responsible financial management and improves the chances of approval, even for secured loans such as home loans and loans against property. Borrowers with higher scores often receive lower interest rates, faster approvals, and better loan terms. Although collateral reduces lender risk, banks still evaluate the applicant’s credit history before sanctioning the loan. In India, a CIBIL score of 750 or above is widely considered good for most loans. Maintaining timely repayments and low credit utilization helps improve your score over time.

Conclusion

Understanding the difference between secured and unsecured loan with examples helps you make informed financial decisions. Secured loans offer lower interest rates and larger loan amounts because they are backed by collateral. Unsecured loans provide quick access to funds without requiring assets but usually come with higher interest rates.

Before applying for any loan, compare lenders, check your CIBIL score, evaluate interest rates, and understand the repayment terms. Choosing the right loan based on your needs and financial situation can help you manage debt effectively and achieve your goals.