Buying a house is one of the biggest financial decisions which most people make in their lifetime. While getting a home loan has become easier, choosing the right loan amount is still a big challenging. Many borrowers focus only on bank eligibility and forget to ask an important question: How much home loan can I truly afford?

This is where the 3-20-30-40 Rule for Home Loan becomes useful.

This simple home loan affordability rule helps you decide:

- How expensive a house you should buy

- How much down payment you should make

- How long your loan tenure should be

- How much EMI you can comfortably afford

Following this rule can help you avoid financial stress, reduce interest costs, and maintain a healthy financial future.

Before taking a home loan, you may also want to read our beginner guide:

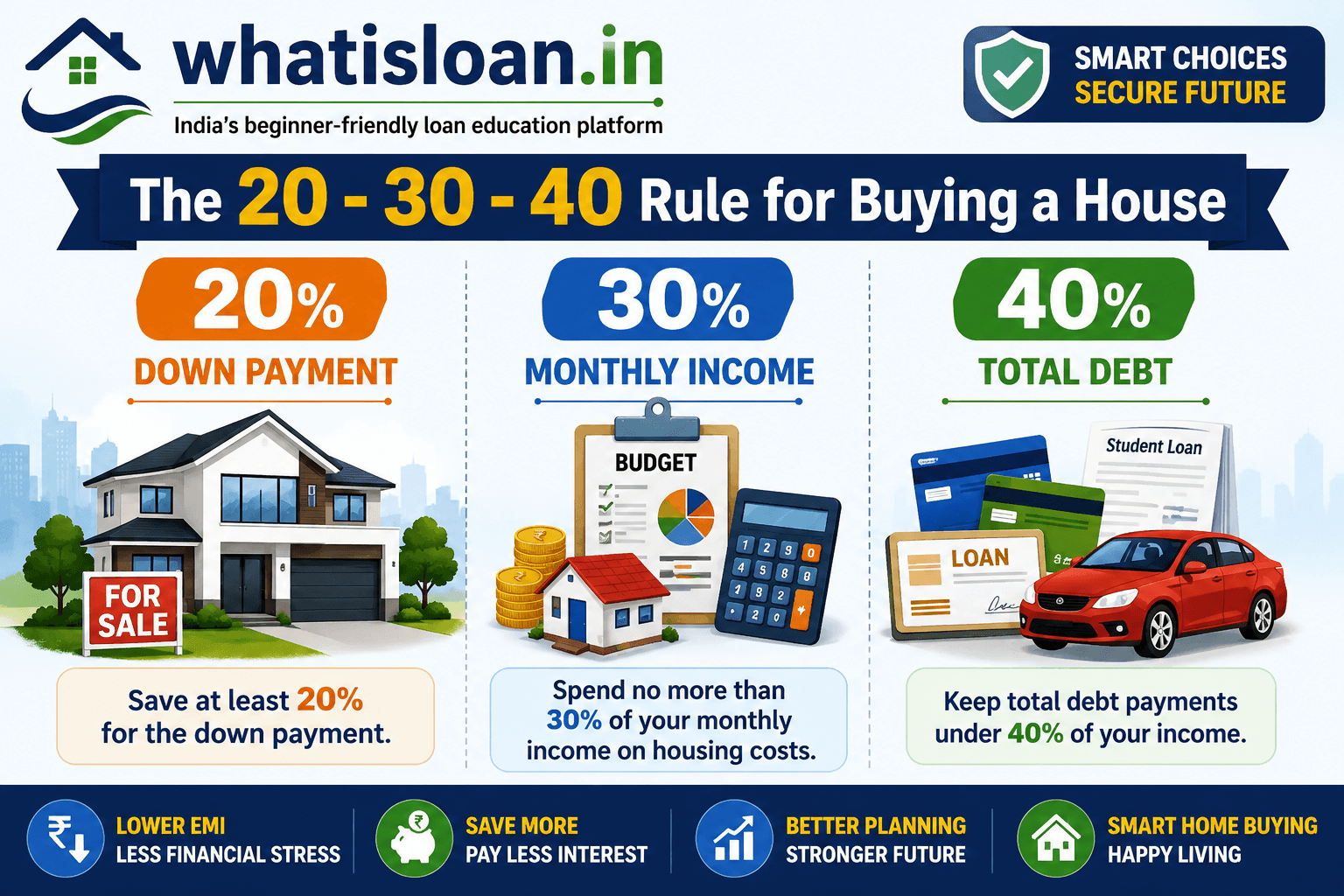

What Is the 3-20-30-40 Rule for Home Loans?

The 3-20-30-40 Rule for Home Loan is a financial planning framework that helps buyers purchase a house without creating long-term financial stress.

It is not:

- An RBI guideline

- A government rule

- A banking regulation

Instead, it is a practical affordability formula recommended by many financial planners.

The goal is simple:

Buy a home you can comfortably afford instead of buying the biggest house a bank is willing to finance.

Why Home Buyers Need the 3-20-30-40 Rule

Many banks approve home loans based on eligibility formulas.

However, eligibility and affordability are not the same thing.

A bank may approve a ₹70 lakh loan, but that does not necessarily mean you can comfortably repay it for 20–30 years.

Common problems faced by borrowers include:

- High EMIs

- Insufficient savings

- Rising interest rates

- Emergency expenses

- Job loss risk

- Poor work-life balance due to financial pressure

The 3-20-30-40 Rule for Home Loan helps avoid these issues.

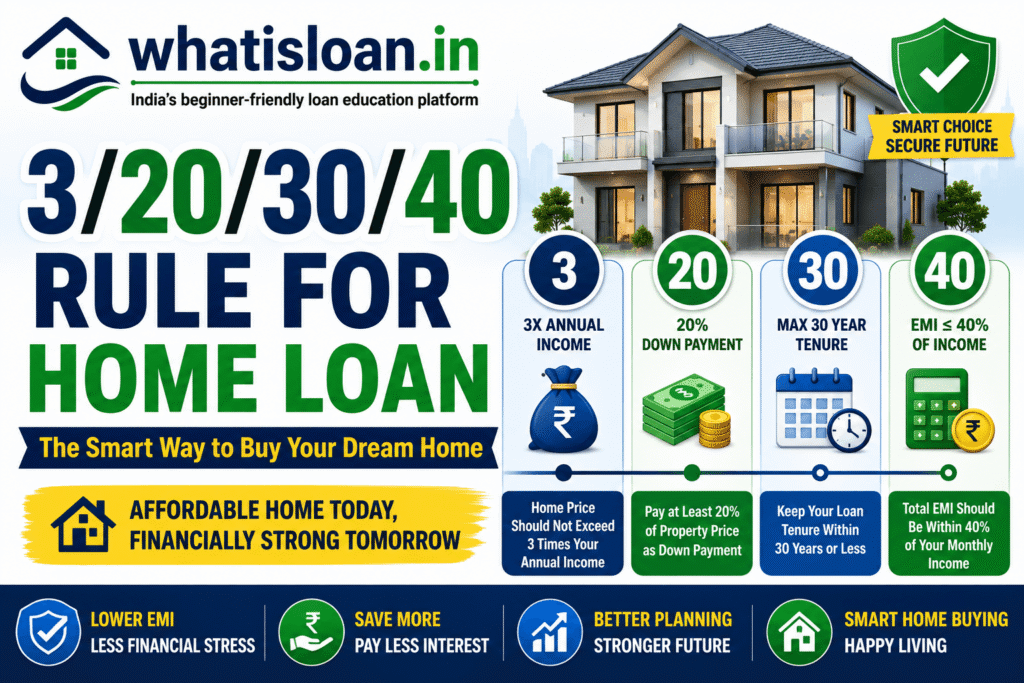

Understanding the 3-20-30-40 Rule

| Number | Meaning |

|---|---|

| 3 | Home price should not exceed 3 times annual income |

| 20 | At least 20% down payment |

| 30 | Loan tenure should ideally not exceed 30 years |

| 40 | Total EMI should stay within 40% of monthly income |

Each part of the rule protects you from a different financial risk.

The 3X Income Rule Explained

What Does “3” Mean?

The first number represents the maximum property value you should target.

Formula

Property Value ≤ 3 × Annual Income

Example

Annual Income = ₹10 Lakh

Maximum Home Price = ₹30 Lakh

Annual Income = ₹20 Lakh

Maximum Home Price = ₹60 Lakh

This rule prevents buyers from purchasing houses that are beyond their long-term affordability.

Why the 3X Rule Matters

Many people purchase properties based on emotions.

Common reasons include:

- Social pressure

- Family expectations

- Larger homes

- Better locations

However, a larger home often means:

- Higher EMI

- Higher maintenance costs

- Less savings

- Greater financial pressure

The 3X rule creates a safe financial boundary.

The 20% Down Payment Rule

What Does “20” Mean?

You should ideally contribute at least 20% of the property value from your own funds.

Example

Property Price = ₹70 Lakh

20% Down Payment = ₹14 Lakh

Loan Amount = ₹56 Lakh

This immediately reduces your borrowing requirement.

Why 20% Down Payment Is Important

Lower Loan Amount

The higher your down payment, the lower your loan.

A smaller loan means:

- Lower EMI

- Lower interest cost

- Faster repayment

Better Loan Approval Chances

Many lenders prefer borrowers who contribute meaningful equity.

A strong down payment reduces lender risk.

Protection Against Market Risks

Property prices do not always increase.

A healthy down payment helps protect you from:

- Negative equity

- Forced sales

- Refinancing difficulties

Hidden Costs Most Buyers Forget

Many first-time buyers focus only on the property price.

However, additional expenses may include:

| Expense | Approximate Cost |

| Stamp Duty | 5%–8% |

| Registration | 1%–2% |

| GST (under construction) | 5% |

| Legal Charges | 0.5%–1% |

| Interior Work | 5%–10% |

Always budget for these costs separately.

You can learn more about home loan documentation here:

The 30-Year Home Loan Rule

What Does “30” Mean?

The third number refers to home loan tenure.

Ideally, your loan tenure should not exceed 30 years.

Many experts actually prefer:

- 15 years

- 20 years

- 25 years

because shorter loans reduce interest costs.

Why Longer Tenures Can Be Expensive

A longer loan tenure:

✓ Lowers EMI

But also:

✗ Increases total interest paid

For example:

| Loan Amount | Tenure | Interest Cost |

| ₹50 Lakh | 20 Years | Lower |

| ₹50 Lakh | 30 Years | Much Higher |

This is why many financial advisors recommend borrowing only what you truly need.

Should You Choose Fixed or Floating Interest Rates?

Most Indian home loans are floating-rate loans.

Understanding interest rate types is important.

Read: https://whatisloan.in/fixed-vs-floating-interest-rate/

The 40% EMI Rule

What Does “40” Mean?

This is arguably the most important part of the 3/20/30/40 Rule for Home Loan.

Your total monthly EMI obligations should not exceed 40% of your gross monthly income.

This includes:

- Home Loan EMI

- Car Loan EMI

- Personal Loan EMI

- Education Loan EMI

- Credit Card EMI

Example

Monthly Income = ₹1,00,000

Maximum Total EMI = ₹40,000

Anything above this level may create financial stress.

Why the 40% Rule Is Critical

Life is unpredictable.

You may face:

- Medical emergencies

- Job loss

- Family expenses

- School fees

- Unexpected repairs

Keeping EMI within 40% ensures you have enough room to handle life’s surprises.

Banks vs Financial Reality

| EMI Ratio | Bank View | Real Life |

| 50–60% | Often Approved | High Risk |

| 40% | Acceptable | Moderate Risk |

| 30% | Ideal | Comfortable |

Remember:

Just because a bank approves a loan does not mean you should take it.

Practical Example: How the 3-20-30-40 Rule Works

Let’s understand the complete 3-20-30-40 Rule for Home Loan using a real-life example.

Buyer Profile

- Monthly Income: ₹1,50,000

- Annual Income: ₹18,00,000

- Existing Car Loan EMI: ₹10,000

- Credit Score: 780

Step 1: Apply the 3X Income Rule

Annual Income = ₹18 Lakh

Maximum House Price = ₹18 Lakh × 3

= ₹54 Lakh

According to the affordability rule, this buyer should ideally target a property worth around ₹54 lakh.

Step 2: Apply the 20% Down Payment Rule

Property Price = ₹54 Lakh

20% Down Payment = ₹10.8 Lakh

Required Loan = ₹43.2 Lakh

This immediately reduces the borrowing requirement and saves interest.

Step 3: Apply the 30-Year Tenure Rule

A loan tenure between:

- 20 years

- 25 years

- 30 years

can be considered.

However, shorter tenures generally save more interest.

Step 4: Apply the 40% EMI Rule

Monthly Income = ₹1,50,000

Maximum Total EMI = 40%

= ₹60,000

Existing Car EMI = ₹10,000

Remaining EMI Capacity = ₹50,000

This means the buyer should keep the home loan EMI below ₹50,000.

The result:

✔ Affordable property

✔ Manageable EMI

✔ Lower financial stress

✔ Better savings potential

Benefits of Following the 3-20-30-40 Rule for Home Loan

The biggest advantage of the 3-20-30-40 Rule for Home Loan is financial peace of mind.

1. Prevents Over-Borrowing

Many borrowers take the maximum loan offered by the bank.

This often results in:

- High EMIs

- Low savings

- Financial stress

The affordability rule helps you borrow responsibly.

2. Reduces Interest Burden

A higher down payment means:

- Smaller loan amount

- Lower interest cost

- Faster loan closure

Over a 20–30 year period, this can save several lakhs of rupees.

3. Protects Emergency Savings

Your financial life does not stop after buying a house.

You still need money for:

- Medical emergencies

- Children’s education

- Retirement planning

- Travel

- Home maintenance

The 40% EMI limit helps protect your cash flow.

4. Improves Financial Stability

A manageable home loan helps maintain balance between:

- Living expenses

- Savings

- Investments

- Debt repayment

This creates long-term financial stability.

5. Reduces Credit Score Risk

Missing EMIs can negatively affect your credit score.

A lower credit score can make it difficult to obtain:

- Personal loans

- Business loans

- Credit cards

- Future home loans

Learn how credit scores work:

6. Makes Interest Rate Increases Easier to Handle

Most Indian home loans have floating interest rates.

When interest rates rise:

- EMI may increase

- Loan tenure may increase

Borrowers already operating near their financial limits often struggle.

A conservative borrowing strategy provides flexibility.

You can learn more about difference between fixed and floating interest rate here:

Common Mistakes Home Buyers Make

Even financially aware buyers sometimes make mistakes.

Mistake 1: Buying Based on Bank Eligibility

Banks often approve larger loans than what is comfortable.

Remember:

Loan eligibility is not the same as loan affordability.

Mistake 2: Ignoring Hidden Costs

Many buyers only focus on the property’s listed price.

Additional expenses include:

- Stamp Duty

- Registration Fees

- Interior Design

- Furniture

- Legal Charges

- Maintenance Deposits

These costs can easily add 10–15% to your budget.

Mistake 3: Using Bonuses to Calculate EMI Capacity

Never rely on:

- Bonuses

- Incentives

- Variable pay

- Freelance income

Use only your stable income when calculating affordability.

Mistake 4: Taking a Home Loan Without Emergency Savings

Before buying a house, try to maintain:

- 6–12 months of expenses

- Emergency fund

- Health insurance coverage

Home ownership should not eliminate your financial safety net.

Mistake 5: Ignoring Existing Debt

Many buyers already have:

- Personal loans

- Car loans

- Credit card EMIs

All these obligations count toward the 40% rule.

To understand different loan types, read here:

Who Should Follow the 3-20-30-40 Rule Strictly?

While the rule is useful for everyone, some groups should follow it more carefully.

First-Time Home Buyers

First-time buyers often underestimate ownership costs.

The rule creates a safe financial framework.

Single-Income Families

When only one person earns, income disruption can create serious challenges.

Following the affordability rule reduces risk.

Salaried Employees

Job changes, layoffs, and economic uncertainty can affect income stability.

A conservative loan amount provides protection.

Middle-Class Families

For most middle-income households, a home loan is the largest debt they will ever take.

Using the 3-20-30-40 rule helps avoid becoming “house rich but cash poor.”

Can You Bend the Rule?

The answer is yes—but only slightly.

Situation: Dual Income Family

If both spouses earn stable incomes, there may be some flexibility.

However:

- Both incomes should be reliable

- Emergency savings should be maintained

Situation: High-Income Professionals

High earners may have more flexibility if:

- They have significant savings

- They maintain investments

- Their careers are stable

Situation: Rental Income

Future rental income should never be fully relied upon.

Vacancies and market fluctuations can occur.

Situation: Variable Income

Business owners and freelancers should be more conservative, not less.

Income uncertainty increases financial risk.

If you’re self-employed, wanted to know about the busness loan you may also want to read:

3-20-30-40 Rule vs Bank Eligibility

| Factor | Bank Eligibility | 3-20-30-40 Rule |

|---|---|---|

| Goal | Maximum Loan Approval | Comfortable Repayment |

| Focus | Lending Capacity | Financial Stability |

| Risk | Higher | Lower |

| EMI Burden | Often Higher | Controlled |

| Long-Term Stress | Possible | Reduced |

This comparison highlights why affordability matters more than eligibility.

Key Takeaways

- The 3-20-30-40 Rule for Home Loan is a practical affordability framework.

- Your house price should ideally not exceed three times your annual income.

- Aim for at least a 20% down payment.

- Keep loan tenure within 30 years or less.

- Total EMIs should not exceed 40% of your monthly income.

- The rule helps reduce financial stress and improve long-term stability.

- Home ownership should improve your life, not create constant financial pressure.

Conclusion

Buying a house is a dream for many Indians, but the excitement of ownership should not come at the cost of financial stress.

The 3-20-30-40 Rule for Home Loan offers a simple and practical way to evaluate affordability before signing a loan agreement.

It encourages:

- Responsible borrowing

- Better financial planning

- Lower debt burden

- Healthier cash flow

- Greater peace of mind

Remember, the best home loan is not the largest loan you qualify for—it is the loan you can comfortably repay while still achieving your other financial goals.

Before applying for a home loan, compare lenders, review your budget, check your credit score, and plan carefully.

You may also find these resources helpful:

- https://whatisloan.in/best-banks-for-home-loans-in-india/

- https://whatisloan.in/home-loan-documents-checklist/

- https://whatisloan.in/what-is-a-home-loan-complete-beginners-guide/

Frequently Asked Questions (FAQ)

What is the 3-20-30-40 rule for home loans?

The 3-20-30-40 rule is a financial planning guideline used to determine whether a home purchase is affordable. According to this rule, the property value should ideally not exceed three times your annual household income. Buyers should aim to make a minimum 20% down payment, choose a loan tenure of up to 30 years, and keep total monthly debt obligations, including the home loan EMI, below 40% of their gross monthly income. This framework helps maintain financial stability, reduces the risk of loan stress, and ensures enough cash flow for savings, investments, and daily expenses. While not an official banking rule, many financial planners use this approach to help homebuyers make responsible borrowing decisions.

Is the 3-20-30-40 rule mandatory?

No, the 3-20-30-40 rule is not mandatory. It is neither a legal requirement nor an RBI guideline. Instead, it serves as a practical framework for assessing home affordability. Banks evaluate home loan eligibility based on income, credit score, repayment history, existing liabilities, and other factors. Even if you qualify for a larger loan, following this rule helps reduce financial pressure and improves long-term financial health. Homebuyers often use this guideline to avoid overborrowing and maintain a balance between housing costs and other financial goals.

Can I buy a house worth more than three times my annual income?

Yes, you can purchase a house worth more than three times your annual income if you meet the lender’s eligibility requirements. Many borrowers choose higher-value properties based on future income expectations or additional family income. However, a larger loan amount usually results in higher EMIs and greater financial commitments. Before stretching your budget, consider factors such as emergency savings, future expenses, children’s education, retirement planning, and job stability. Staying within a comfortable affordability range helps reduce financial stress and improves your ability to manage unexpected expenses.

Why is a 20% down payment recommended?

A 20% down payment is often recommended because it reduces the amount you need to borrow. A lower loan amount leads to smaller EMIs and lower total interest costs over the loan tenure. It also improves your loan-to-value ratio, which lenders often view positively during the approval process. Making a larger down payment demonstrates financial discipline and reduces the risk of becoming overleveraged. Although many lenders offer home loans with lower down payment requirements, contributing at least 20% can improve affordability and reduce your overall borrowing burden.

Can my EMI exceed 40% of my income?

Yes, some lenders may approve a home loan where the EMI exceeds 40% of your monthly income, especially if you have a strong credit profile and stable earnings. However, financial experts generally consider this risky because a large portion of your income becomes tied to debt repayment. Higher EMIs can make it difficult to manage household expenses, investments, emergency funds, and lifestyle goals. Keeping total debt obligations below 40% of your income provides greater financial flexibility and reduces the risk of payment difficulties during unexpected situations.

Does the rule apply to joint home loans?

Yes, the 3-20-30-40 rule can be applied to joint home loans. In such cases, you should calculate affordability using the combined income of all co-borrowers. This often increases borrowing capacity and improves loan eligibility. The property value, down payment, loan tenure, and EMI affordability calculations can all be based on total household income. Joint home loans are commonly taken by spouses and family members to improve loan approval chances and share repayment responsibilities. Even with combined income, it is important to ensure the EMI remains comfortable for all borrowers involved.

Should I include bonuses when calculating affordability?

Financial experts generally recommend using only stable and predictable income when calculating home affordability. Regular salary income is a more reliable measure than bonuses, incentives, commissions, or variable earnings. Since bonus payments can fluctuate from year to year, depending on them for home loan affordability may create financial stress if future payouts are lower than expected. Using conservative income estimates provides a more realistic view of your repayment capacity and helps ensure that your home loan remains manageable throughout the loan tenure.

Is a 30-year home loan bad?

A 30-year home loan is not necessarily bad and can be a useful option for improving affordability. A longer loan tenure reduces the monthly EMI, making it easier to fit repayments within your budget. This can be particularly helpful for first-time homebuyers or those purchasing higher-value properties. However, the trade-off is that you pay interest for a longer period, resulting in a significantly higher total interest outflow over the life of the loan. Many borrowers choose longer tenures initially and then make prepayments later to reduce interest costs and shorten the repayment period

Planning to buy a house?

Explore our complete Home Loan Guides, CIBIL Score resources, and Home Loan Planning articles at WhatIsLoan.in to make smarter borrowing decisions and avoid costly mistakes.

**Disclaimer:** The information provided on WhatIsLoan.in is for educational and informational purposes only. We do not provide financial, legal, tax, investment, or loan approval services. Loan eligibility, interest rates, terms, and policies may vary by lender and can change over time. Readers should verify information with banks, NBFCs, government authorities, or qualified financial advisors before making any financial decisions. WhatIsLoan.in is not responsible for any losses or decisions made based on the information published on this website.