Buying a house is one of the biggest financial decisions most people make in their lifetime. Unfortunately, many borrowers make costly mistakes while applying for a home loan. These home loan mistakes can increase your EMI, raise your interest costs, and create financial stress for years.

Understanding the most common home loan mistakes to avoid can help you save lakhs of rupees over the life of your loan. Whether you are a first-time home buyer or planning to upgrade your home, this guide explains the most important things to check before applying for a home loan and how to make smarter borrowing decisions. The ideas in this article are based on expert home loan advice and practical borrower experiences.

Before you continue, you may also want to read our complete guide on Home Loans:

Why Home Loan Planning Matters

A home loan usually lasts between 15 and 30 years.

That means one financial decision today can affect:

- Your monthly budget

- Savings goals

- Children’s education planning

- Retirement planning

- Lifestyle choices

Many borrowers focus only on whether the bank approves their loan.

The smarter question is:

Can I comfortably repay this loan for the next 20 years?

A useful affordability framework is the 3/20/30/40 Rule for Home Loans, which helps determine how much home loan you can safely afford.

Home Loan Mistake #1: Choosing a Longer Tenure Just for a Lower EMI

Why This Mistake Is Common

Many borrowers choose a 25-year or 30-year loan simply because the EMI looks lower.

Banks often promote longer tenures because:

- Lower EMI appears attractive

- Loan eligibility increases

- Total interest paid increases

However, a lower EMI does not always mean a cheaper loan.

Example: ₹50 Lakh Home Loan

| Loan Amount | Interest Rate | Tenure | Approx Total Repayment |

|---|---|---|---|

| ₹50 Lakh | 8% | 20 Years | Around ₹1 Crore |

| ₹50 Lakh | 8% | 30 Years | Around ₹1.32 Crore |

By extending the tenure by just 10 years, you could pay more than ₹30 lakh extra in interest.

Better Approach

Experts generally recommend:

- 15 years (ideal)

- 20 years (good balance)

- 25 years (acceptable)

Choose the shortest tenure you can comfortably afford.

Home Loan Mistake #2: Ignoring Your CIBIL Score

Why Your CIBIL Score Matters

Your credit score tells lenders how responsibly you have handled loans and credit cards in the past.

Today, many banks offer:

- Better interest rates

- Faster approvals

- Higher loan eligibility

to borrowers with strong credit profiles.

Recommended CIBIL Score Range

| CIBIL Score | Loan Approval Chances |

| 750+ | Excellent |

| 700–749 | Good |

| 650–699 | Average |

| Below 650 | Difficult |

What to Check Before Applying

- Check your CIBIL score

- Correct reporting errors

- Pay credit card dues

- Avoid loan defaults

A strong credit profile can improve your chances of approval and help you secure better interest rates. Learn more about the ideal CIBIL score for a home loan.

Home Loan Mistake #3: Not Comparing Interest Rates Across Banks

Many buyers apply to the first bank that offers a loan.

This can be a costly mistake.

Even a small difference of:

- 0.25%

- 0.50%

- 1%

can save lakhs of rupees over time.

To check the difference in Interest rate you need to use Interest Rate Comparison Calculator, which will you total saving on you hard earn money.

Compare Multiple Lenders

Before choosing a lender, compare:

- Interest rates

- Processing fees

- Prepayment rules

- Foreclosure charges

- Customer service

Home Loan Mistake #4: Choosing the Wrong Interest Rate Type

Fixed vs Floating Interest Rates

One of the most important things to check before applying for a home loan is the type of interest rate.

Fixed Rate

Pros:

- Predictable EMI

- Budget certainty

Cons:

- Usually higher interest rates

- Less benefit when rates fall

Floating Rate

Pros:

- Usually lower rates

- Benefit when RBI reduces rates

Cons:

- EMI or tenure may change

According to most experts, floating-rate home loans are generally preferred because they usually offer lower rates and better long-term flexibility.

Home Loan Mistake #5: Ignoring Prepayment Opportunities

What Is Home Loan Prepayment?

Prepayment means paying extra money toward your home loan principal before the scheduled EMI.

Sources may include:

- Annual bonus

- Salary increment

- Incentives

- Rental income

- Investments

Why Prepayment Is Powerful

In the early years of a home loan:

- Most EMI goes toward interest

- Principal reduction is slow

Making occasional prepayments can dramatically reduce:

- Loan tenure

- Total interest paid

For example, a ₹5 lakh prepayment on a ₹50 lakh loan can reduce several years from your loan tenure and save significant interest costs.

Home Loan Mistake #6: Not Understanding Hidden Charges

Many borrowers focus only on interest rates.

However, there are other costs involved.

Common charges include:

- Processing Fees

- Legal Verification Charges

- Technical Evaluation Fees

- Documentation Charges

- Insurance Charges

- Foreclosure Charges

Always ask for a complete fee breakdown before signing any agreement.

Home Loan Documents You Should Verify

Before applying, ensure you have:

- PAN Card

- Aadhaar Card

- Income Proof

- Bank Statements

- Property Documents

- Passport-size Photos

Missing paperwork is one of the most common reasons for delays. Use our Home Loan Documents Checklist before applying.

Home Loan Mistake #7: Borrowing More Than You Can Afford

Just Because a Bank Approves It Doesn’t Mean You Should Take It

One of the biggest home loan mistakes to avoid is assuming that the bank’s approved loan amount is the right amount for you.

Banks calculate eligibility based on:

- Income

- Existing liabilities

- Credit score

- Age

- Employment profile

However, banks do not always consider your future financial goals.

For example:

- Children’s education

- Retirement planning

- Medical emergencies

- Family responsibilities

- Lifestyle expenses

A bank may approve a ₹75 lakh loan, but that does not mean you should take the entire amount.

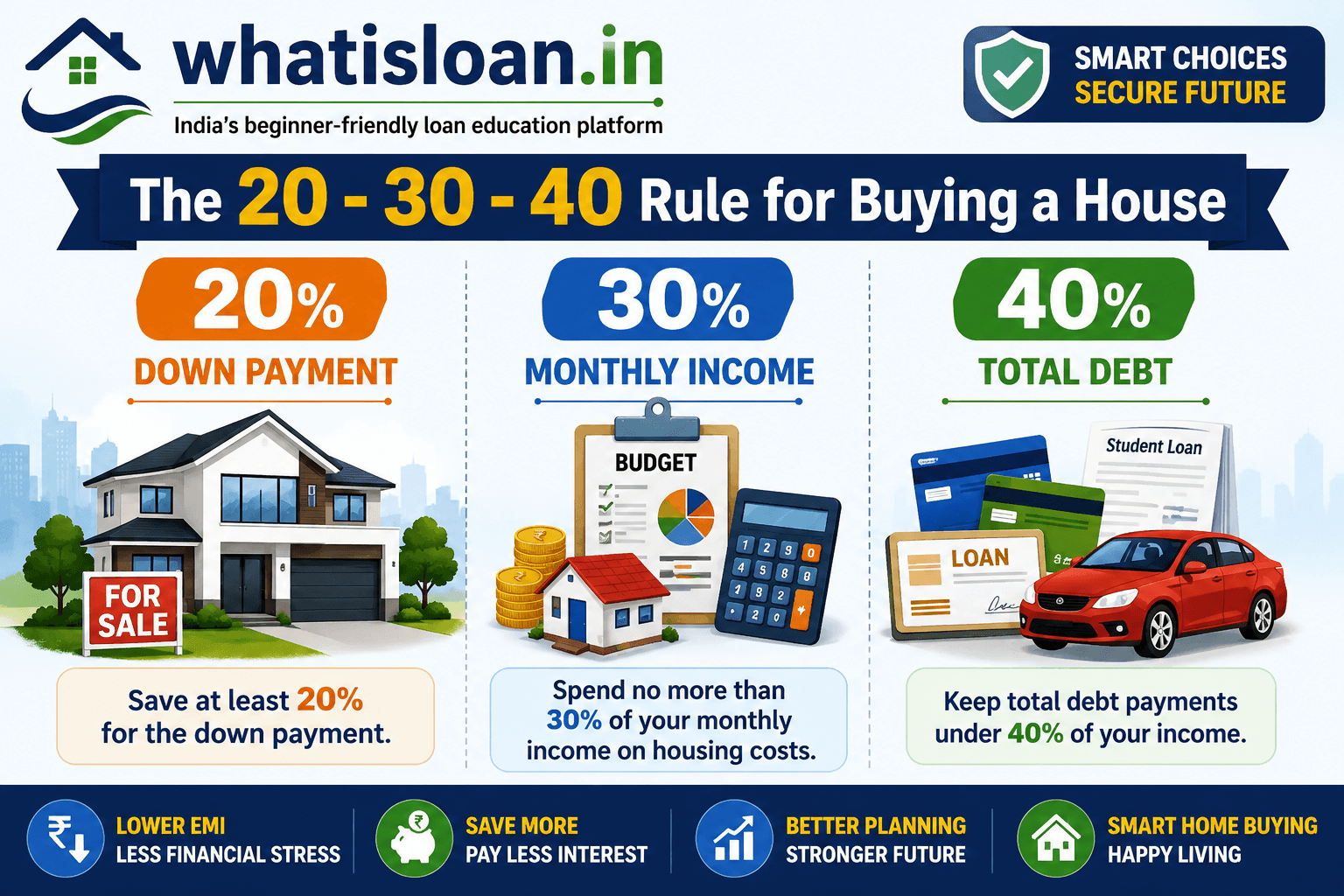

Follow a Home Loan Affordability Rule

A safer approach is to use the 3/20/30/40 Rule for Home Loans.

This rule suggests:

| Rule | Meaning |

|---|---|

| 3 | House price should ideally not exceed 3 times annual income |

| 20 | Minimum 20% down payment |

| 30 | Prefer loan tenure around 20–30 years |

| 40 | Total EMI should stay below 40% of monthly income |

A useful affordability framework is the 3/20/30/40 Rule for Home Loans, which helps determine how much home loan you can safely afford.

Home Loan Mistake #8: Not Keeping an Emergency Fund

Why This Is Dangerous

Many people use all their savings for:

- Down payment

- Registration fees

- Stamp duty

- Interiors

- Furniture

After purchasing the house, they have almost no emergency savings left.

This can create serious problems if:

- You lose your job

- A medical emergency occurs

- Family expenses increase

- Interest rates rise

Recommended Emergency Fund

Experts generally recommend maintaining:

| Situation | Emergency Fund |

| Salaried Employee | 6 Months Expenses |

| Self-Employed | 12 Months Expenses |

Your emergency fund should remain untouched even after buying a house.

Home Loan Mistake #9: Ignoring Property Verification and Documents

Why Property Documents Matter

Many buyers focus entirely on loan approval and ignore property verification.

This can lead to:

- Legal disputes

- Ownership issues

- Delayed possession

- Loan rejection

Important Documents to Verify

Before finalizing any property, verify:

Title Deed

Confirms ownership.

Sale Agreement

Shows purchase terms.

Approved Building Plan

Ensures legal construction.

Occupancy Certificate (OC)

Confirms the building is fit for occupation.

Completion Certificate (CC)

Shows construction compliance.

Property Tax Receipts

Confirms tax payments.

Use a Home Loan Documents Checklist

Before applying, review our complete Home Loan Documents Checklist:

Proper documentation can speed up approval and reduce stress.

Home Loan Mistake #10: Ignoring Hidden Charges and Fees

Interest Rate Is Not the Only Cost

Many borrowers compare only interest rates.

However, banks may charge additional fees.

Common home loan charges include:

| Charge Type | Description |

| Processing Fee | Loan application fee |

| Legal Fee | Property verification |

| Technical Fee | Property valuation |

| Documentation Fee | Paperwork costs |

| Insurance Premium | Optional or bundled coverage |

| Foreclosure Charge | Early loan closure charges (in some cases) |

Questions You Should Ask Before Signing

Ask your lender:

- What is the processing fee?

- Are there legal verification charges?

- Is insurance mandatory?

- Are there foreclosure charges?

- Are there prepayment penalties?

A small hidden charge today can become a significant cost later.

Home Loan Mistake #11: Applying Without Proper Research

Don’t Rush Into a Home Loan

Many buyers:

- Visit one bank

- Accept the first offer

- Sign documents quickly

This can be expensive.

Compare Multiple Lenders

Before applying, compare:

- Interest rates

- Processing fees

- Customer reviews

- Loan features

- Online services

- Prepayment rules

You can start by reviewing the Best Banks for Home Loans in India:

Understand Loan Types

Understanding the difference between Secured and Unsecured Loans can help you become a better borrower overall.

Quick Home Loan Checklist Before Applying

| Home Loan Checklist Before Applying | Status |

|---|---|

| Check your CIBIL Score (750+ preferred) | ✅ |

| Compare Interest Rates from Multiple Banks | ✅ |

| Verify Property Documents Carefully | ✅ |

| Calculate Home Loan EMI Affordability | ✅ |

| Maintain an Emergency Fund (6–12 Months) | ✅ |

| Compare Fixed vs Floating Interest Rates | ✅ |

| Understand Processing Fees & Hidden Charges | ✅ |

| Review Prepayment and Foreclosure Rules | ✅ |

| Collect All Required Home Loan Documents | ✅ |

| Read the Loan Agreement Thoroughly | ✅ |

| Check Home Loan Eligibility Criteria | ✅ |

| Confirm Down Payment Availability | ✅ |

| Review Loan Tenure Options | ✅ |

| Compare Customer Service and Loan Support | ✅ |

| Ensure Monthly EMI Fits Your Budget | ✅ |

Key Takeaways

- Avoid choosing a longer loan tenure only for a lower EMI.

- Check your CIBIL score before applying.

- Compare multiple lenders and interest rates.

- Understand the difference between fixed and floating interest rates.

- Make prepayments whenever possible.

- Review all hidden charges carefully.

- Borrow only what you can comfortably repay.

- Keep an emergency fund after purchasing your home.

- Verify all property documents.

- Never rush into signing a home loan agreement.

Frequently Asked Questions (FAQ)

What is the biggest mistake people make when taking a home loan?

One of the biggest mistakes homebuyers make is choosing a longer loan tenure solely to reduce their monthly EMI. While a lower EMI may seem attractive, extending the tenure significantly increases the total interest paid over the life of the loan. Many borrowers focus only on monthly affordability and ignore the long-term cost of borrowing. Other common mistakes include not comparing multiple lenders, ignoring processing fees and hidden charges, borrowing more than necessary, and failing to maintain an emergency fund after making the down payment. Before applying, carefully assess your repayment capacity, future financial goals, and overall loan cost. A well-planned home loan can save lakhs of rupees in interest and reduce financial stress during the repayment period.

How much CIBIL score is required for a home loan?

Most lenders prefer a CIBIL score of 750 or above when evaluating home loan applications. A higher credit score indicates responsible credit behavior and improves your chances of loan approval. Borrowers with strong credit scores often qualify for better interest rates, higher loan amounts, and faster processing. While some lenders may approve applications with lower scores, the interest rate may be higher, increasing the overall borrowing cost. Maintaining timely EMI payments, keeping credit card utilization low, and avoiding frequent loan applications can help improve your score over time.

Is prepayment good for a home loan?

Yes, prepayment is generally one of the most effective ways to reduce the overall cost of a home loan. When you make a partial prepayment, the outstanding principal decreases, which reduces the interest charged on the remaining balance. This can help shorten the loan tenure and save a substantial amount of interest over time. The greatest benefit is usually seen during the early years of the loan because a larger portion of the EMI goes toward interest payments. Many borrowers use bonuses, salary increments, rental income, or investment gains to make periodic prepayments. Before making a prepayment, check whether your lender imposes any charges and understand how the payment will affect your loan schedule.

Which is better: fixed or floating interest rate?

The choice between a fixed and floating interest rate depends on your financial goals, risk tolerance, and market conditions. Fixed-rate home loans provide stability because the interest rate remains unchanged for a specified period, making budgeting easier. Floating-rate loans, on the other hand, move in line with market interest rates and may increase or decrease over time. Historically, floating rates have often been lower than fixed rates, making them a popular choice among borrowers. However, rising interest rates can increase EMI amounts or extend the loan tenure. Understanding the advantages and disadvantages of both options is essential before making a decision.

What documents should I check before applying?

Preparing the correct documents before applying for a home loan can improve approval chances and speed up processing. Most lenders require identity proof, address proof, income proof, salary slips, bank statements, PAN card, Aadhaar card, and property-related documents. Self-employed applicants may also need business registration documents, income tax returns, and audited financial statements. Property documents should be carefully verified to ensure legal ownership and compliance with local regulations. Missing or incorrect paperwork can delay loan approval and create unnecessary complications. Organizing all required documents in advance helps make the application process smoother and more efficient.

How many banks should I compare before applying?

It is generally recommended to compare at least three to five lenders before selecting a home loan. Different banks and housing finance companies offer varying interest rates, processing fees, loan tenures, customer service standards, and prepayment policies. Even a small difference in interest rates can result in significant savings over a long repayment period. Comparing lenders allows you to identify the most competitive offer and avoid paying unnecessary charges. In addition to interest rates, review loan features such as balance transfer options, foreclosure terms, and customer reviews. Spending time on comparison before applying can help you secure better loan terms and reduce your overall borrowing costs.

Should I use all my savings for a down payment?

No, using all your savings for a home loan down payment is generally not recommended. While a larger down payment reduces the loan amount and interest burden, exhausting your savings can leave you financially vulnerable. Homeownership often involves additional expenses such as registration charges, maintenance costs, repairs, insurance premiums, and emergency expenses. Financial experts recommend maintaining an emergency fund that covers at least six months of living expenses even after making the down payment. Having adequate savings provides financial security during unexpected events such as medical emergencies, job loss, or temporary income disruptions. A balanced approach between down payment contribution and emergency savings is usually the safest strategy.

Conclusion

Buying a home is a dream for many Indians, but a home loan should support that dream—not become a long-term financial burden.

The good news is that most costly home loan mistakes are avoidable.

By checking your credit score, comparing lenders, choosing the right tenure, understanding interest rates, reviewing charges, and making smart prepayments, you can save lakhs of rupees over the life of your loan.

Most importantly, borrow based on affordability rather than eligibility.

A comfortable home loan is always better than the biggest home loan you qualify for.

Before applying, take time to plan, compare, and understand every aspect of the loan process.

**Disclaimer:** The information provided on WhatIsLoan.in is for educational and informational purposes only. We do not provide financial, legal, tax, investment, or loan approval services. Loan eligibility, interest rates, terms, and policies may vary by lender and can change over time. Readers should verify information with banks, NBFCs, government authorities, or qualified financial advisors before making any financial decisions. WhatIsLoan.in is not responsible for any losses or decisions made based on the information published on this website.